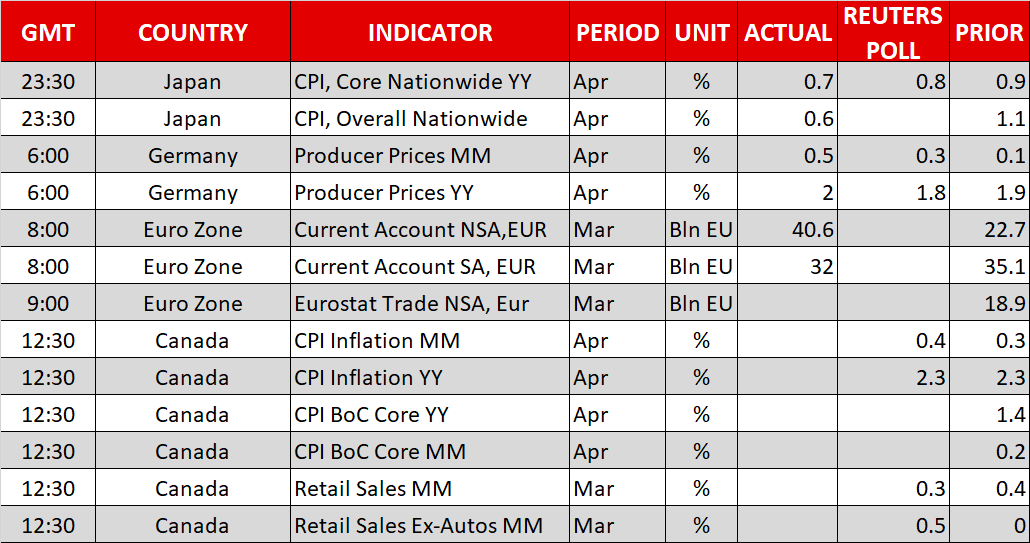

Here are the latest developments in global markets:

Here are the latest developments in global markets:

FOREX: The US dollar index is lower today, but by less than 0.1%, giving back some of the gains it posted yesterday. The yen is on the back foot too, declining more than 0.2% against the euro and 0.05% versus the dollar, following disappointing inflation data out of Japan overnight.

STOCKS: US markets closed in the red on Thursday, weighed on by some remarks from US President Trump that he doubts the US and China can reach a trade agreement. The Dow Jones and the Nasdaq Composite fell by 0.22% and 0.21% respectively, while the S&P 500 declined by 0.09%. Market sentiment looks to have reversed though, as futures tracking the Dow, S&P, and Nasdaq 100 are all currently pointing to a higher open today, something likely owed to reports that China has made the US an offer on trade (see below). In Asia, the Nikkei 225 and the Topix rose by 0.4% and 0.38% correspondingly, while in Hong Kong, the Hang Seng climbed 0.6%. In Europe, futures tracking the major indices were mostly in the red, with the only exceptions being the German DAX and Italian FTSE MIB.

COMMODITIES: Oil prices are higher today, with WTI and Brent crude gaining 0.17% and 0.25% respectively. Both benchmarks touched fresh multi-year highs yesterday. Brent briefly punched through the psychological $80/barrel zone, even though EU leaders signaled their continued support to the Iran deal and discussed ways to block US sanctions on European companies doing business with Iran. In precious metals, gold prices are practically unchanged on Friday, last seen near the $1290 per ounce mark. Ever since the yellow metal broke below the psychological $1300 handle, it has largely traded sideways, reacting little to anything other than moves in the US dollar.

Major movers: Yen on the back foot, China makes the US an offer on trade

The dollar index is marginally lower on Friday, though still remains elevated just below a five-month high. The currency edged higher yesterday, supported by the yields on 10-year US Treasuries remaining elevated near seven-year highs. The dollar’s gains were more pronounced against the yen, which cannot draw support from relative interest rates, as the Bank of Japan (BoJ) is keeping the yields on longer-term Japanese bonds fixed near 0%.

The yen is on the back foot today as well, following disappointing inflation data out of Japan. Both the headline and the core CPI rates declined notably. Coming on top of soft GDP data recently, these prints likely amplified speculation the BoJ will maintain its ultra-loose policy framework in place for longer.

On the trade front, US President Trump indicated on Thursday he doubts trade negotiations with China would be successful, “because China has become very spoiled”. The two sides resumed talks yesterday, which will continue today.

A few hours later though, reports suggested China has presented the US with proposals aimed at reducing the trade deficit between them by $200 billion per year, mainly by increasing Chinese purchases of US goods. While no other details are available yet, it’s also worth noting that overnight, China dropped an anti-dumping tariff it imposed last month on US sorghum imports. Although the Asian nation cited increased costs for its farmers as the reason, the move may have also been “an offering of goodwill”, as the two sides attempt to come to terms on the bigger issues.

Markets will likely be on the lookout for any fresh remarks on the subject today. Any hints from US officials that China’s $200 billion offer is something they can work with could boost risk appetite, potentially pushing equities higher and safe havens lower. The opposite holds true as well.

Dollar/loonie spiked higher overnight following remarks on NAFTA, but has given back most of its gains and is currently only 0.05% higher on the day. The move came after US trade representative Lighthizer said NAFTA countries are nowhere close to a deal, pouring cold water on expectations that a resolution may be achieved before the Mexican election in July.

Day ahead: Canadian inflation & retail sales pending; Trade & North Korea developments in focus

Data out of the Eurozone, Canada and the US are likely to keep investors busy on Friday, while US Treasury yields will be closely watched for signs of gains in the dollar market. Trade headlines and developments in the US-North Korea relations could add volatility to the markets as well.

At 0800 GMT, Eurozone will see the release of trade stats for the month of March and it would be interesting to see whether the bloc’s trade surplus continued to narrow at times when the Eurozone is pushing efforts to eliminate threats of import metal tariffs from the US. Recall that the German Chancellor Angela Merkel said recently that Europe will be prepared to enter discussions on how to reduce trade barriers if the US provides a permanent tariff exception without conditions or time limits. Renewed US sanctions against Iran are also a concern to the region given that Europe is one of Iran’s biggest oil customers after China and India.

The North Korea story will remain in the spotlight as latest comments by the US President and the North Korea leader have eased hopes of a productive US-North Korea summit on June 12. Following threats from North Korea to cancel the summit if Washington pushed for a unilateral denuclearization, Trump answered that North Korea could be “decimated” if it refused to make a deal with the US.

In Canada, the focus will turn to inflation and retail sales readings at 1230 GMT after the US, Canada and Mexico missed Thursday’s deadline to form a NAFTA deal, with the US trade representative Robert Lighthizer stating the member countries are “nowhere near close to a deal”. At the same time, though, the Canadian Prime Minister expressed optimism about talks to save NAFTA, while a Mexican top official spurred hope that an agreement could be reached by the end of May. Canadian consumer prices in April are forecast to have grown at March’s pace of 2.3% y/y, remaining above the midpoint of the Bank of Canada’s 1-3.0% range target for the second consecutive month. A rate hike, however, is less likely to be announced at the end of this month despite a tighter labor market as trade and debt uncertainties continue to loom in the background. Core inflation measures, which trim for volatility and are closely monitored by BoC policymakers will attract attention as well. On the other hand, retail sales for the month of March are anticipated to ease from 0.4% m/m to 0.3% in overall but in the absence of automobiles, the measure is expected to improve to 0.5% after showing no growth in the previous month. In the wake of a positive data surprise, especially in the inflation front as the numbers are more recent, the loonie could strengthen.

In oil markets, Baker Hughes’s weekly report on US oil rig count will be issued at 1700 GMT, with a high potential to move prices.

As for today’s public appearances, Dallas Fed President Robert Kaplan will be participating in moderated question-and-answer session before the 12th Annual University of Texas at Dallas Project Management Symposium at 1315 GMT, while at the same time Fed board Governor Lael Brainard will be speaking on “Community Reinvestment Act Modernization” before the Association for Neighborhood and Housing Development 8th Annual Community Development Conference.

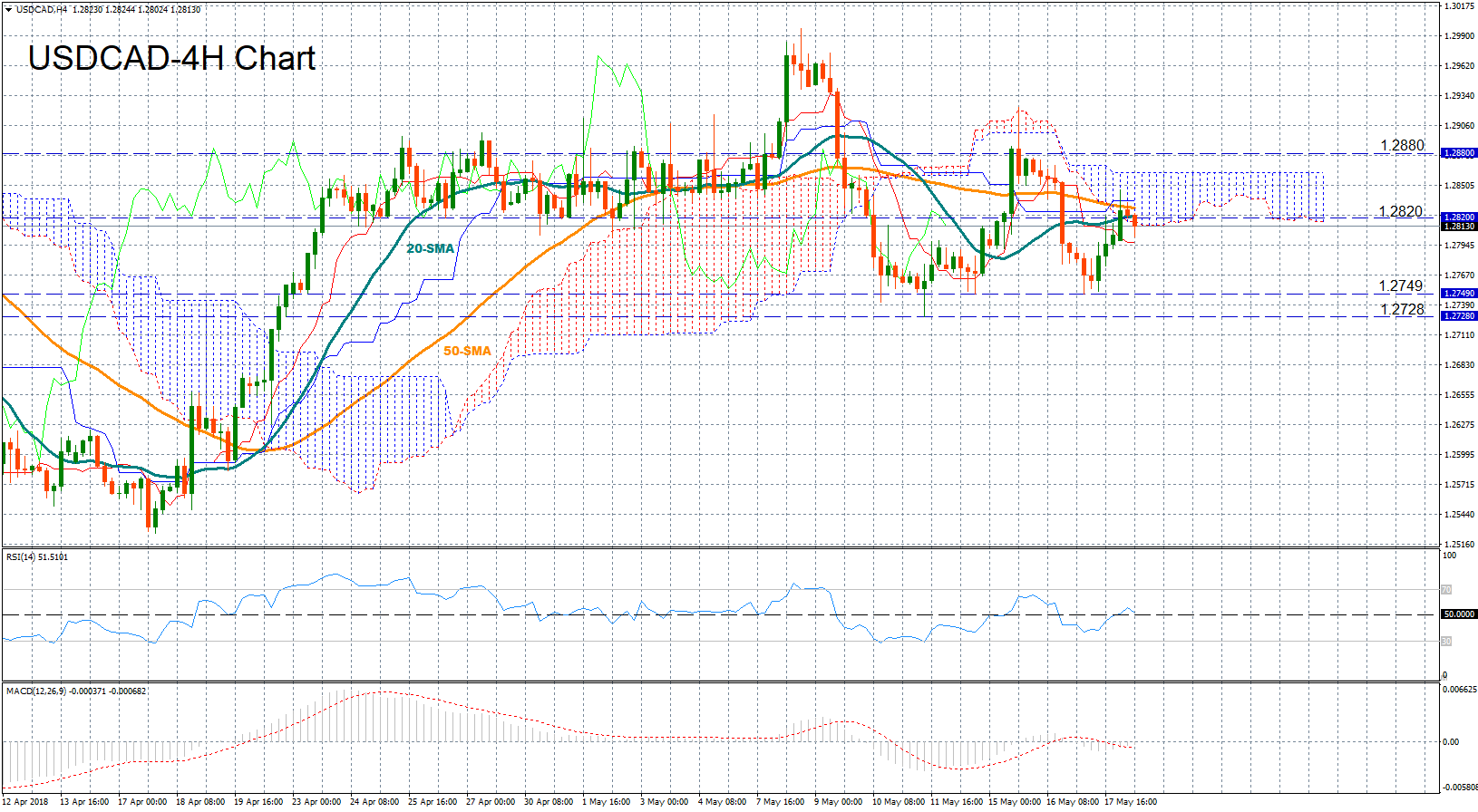

Technical analysis – USDCAD in bearish mode ahead of key-data release

USDCAD managed to restore part of losses made since the start of the week on Thursday but today the pair is heading lower, with technical indicators in the four-hour chart suggesting that the market is less likely to gain momentum in the short-term; the RSI is negatively sloped and on track to cross below its neutral threshold of 50, while the MACD continued to fluctuate marginally below zero.

Still, upbeat inflation and retail sales figures out of Canada later today could boost the loonie, sending the market down to yesterday’s trough of 1.2749. A break below that level could also shift focus towards the low of 1.2711 reached on May 11.

In the alternative scenario, a miss in data could work in favor of the dollar, pushing the market up to the area embraced by the 20- and the 50-day simple moving averages which currently trend between around 1.2820. A bigger surprise, though, could probably run resistance even higher towards 1.2880, a frequently congested area from the end of April onwards.

Origin: XM