Here are the latest developments in global markets:

Here are the latest developments in global markets:

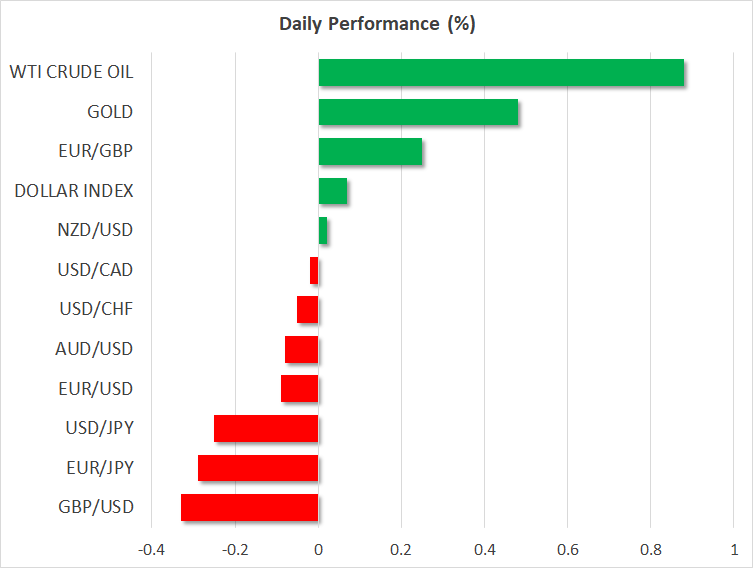

- FOREX: The dollar is marginally higher on Monday against a basket of six major currencies (+0.07%), extending the gains it recorded in the previous session. The safe-haven Japanese yen is the best performer among the G10 currencies, as a diplomatic rift between the US and Saudi Arabia is seemingly keeping investors on the defensive. Elsewhere, the British pound opened with a gap to the downside, after the EU and UK were reported to have paused the Brexit talks until later this week, after failing to reach common ground over the weekend.

- STOCKS: US indices bounced back on Friday, in the absence of any developments in the trade conflict or major movements in the US bond market to speak of. A potential catalyst for the rebound may have been a solid start to the earnings season fueling hopes for yet another blockbuster quarter. Tech stocks outperformed, with the tech-heavy Nasdaq Composite rallying by 2.29%. The S&P 500 (+1.42%) and Dow Jones (+1.15%) followed in its tracks. However, the positive sentiment did not spill over into Asia, which was a sea of red on Monday. In Japan, the Nikkei 225 (-1.87%) and Topix (-1.59%) felt the pain, as a stronger yen clouded the outlook for exporting firms. In Hong Kong, the Hang Seng dropped by 1.34%. Europe was mixed, with futures pointing to a relatively flat open today for most indices.

- COMMODITIES: Oil opened with a gap to the upside, after Saudi Arabia threatened to curtail its crude production in case the US decided to proceed with sanctions over the disappearance of a Saudi journalist (see below). Considering that the Kingdom was expected to raise its production in the face of Iranian sanctions, not rein it in, the news likely caught the oil market by surprise. WTI is up by almost 0.90% at $71.84 per barrel, while Brent gained 0.97% to settle near $81.21. In precious metals, gold is higher by nearly 0.50% on Monday, at $1,227 per ounce. Following the break above the upper bound of the range it had been trading in recently on Thursday, the metal’s short-term technical outlook has shifted to positive.

Major movers: Sterling gaps lower as Brexit talks “paused”; stocks get a reprieve

The British pound opened with a gap lower this week, in the wake of news that the Brexit talks have been “paused” until Wednesday’s EU summit. The reports suggest intense negotiations through the weekend failed to bear fruit, and were called off on Sunday amid a lack of progress on the Irish border issue. This likely poured cold water on any expectations that a deal may be wrapped up as early as this week. It also implies the proverbial can has now been kicked down the road to November, when the EU may call a special summit to discuss Brexit, provided enough headway has been made until then. As for the pound, it will probably remain hostage to incoming headlines, with price action potentially staying choppy and directionless until there is some further clarity on the issue.

In the broader market, US stocks rebounded on Friday in the absence of any major fresh catalyst, as the earnings season kicked off. Encouraging results from banking heavyweights such as JP Morgan and Citigroup may have helped support risk appetite a little, on speculation for another blockbuster earnings season. That said though, it appears this was merely a brief reprieve, as the optimism failed to spill over into Asia on Monday, and futures tracking the major US indices are pointing to a lower open today as well.

The fact that risk sentiment is not out of the woods yet may be (at least partly) owed to an escalating diplomatic rift between the US and Saudi Arabia over the weekend. Tensions flared up after the disappearance of a Washington Post journalist inside Saudi Arabia’s embassy in Turkey, with President Trump threatening “very powerful” sanctions. The Kingdom replied it would hit back with countermeasures, including lowering its oil production to push prices higher, stop buying weapons from the US, and curtailing investments in the US. Oil prices opened higher on the news, while the safe-haven Japanese yen is the best performer among the major currencies, with investors evidently curtailing their risk-taking.

Elsewhere, after flying under the radar over the past few days, market attention could turn back to the Italian budget crisis this week, as today marks the deadline for the highly-controversial budget to be presented to the EU Commission for approval. The EU is nearly certain to reject the budget in its current form, and the tone of the accompanying remarks may be seen as a gauge of whether this will morph into a full-fledged political standoff. The euro will likely move accordingly, lower on signs of further conflict, or higher on anything pointing to a middle-of-the-road compromise being within reach.

Day ahead: US retail sales in focus; Brexit updates eyed

US retail sales due at 1230 GMT are the highlight on Monday’s economic calendar.

US retail sales for September are anticipated to have grown by 0.6% m/m, faster than August’s 0.1%. Additionally, core retail sales, this being the measure of sales that excludes automobiles and which more closely aligns with the consumer spending component of GDP, is projected to grow by 0.4% m/m, above August’s 0.3%. A beat in the numbers has the capacity to stoke expectations for a December 25bps hike by the US central bank (78% probability at the moment according to Fed fund futures), something which is theoretically dollar-positive. The opposite holds true as well.

Meanwhile, the New York Fed manufacturing index for October and numbers on September’s retail control are also due at 1230 GMT, while data on business inventories will follow out of the world’s largest economy at 1400 GMT.

Elsewhere, Brexit developments are anticipated to remain the main sterling driver. Weekend talks failed to provide a breakthrough, weighing on the pound. The EU heads of government summit on October 17-18 is expected to touch on pending issues, most notably the Irish border one, with Brexit headlines possibly hitting the markets even before that.

In equities, Bank of America will be releasing quarterly results before the US market open. The fact Friday’s rebound in stock markets received no traction in Asia today, is an indication that investors remain wary on factors such as trade and rising yields.

Origin: XM