Русский

Русский

Markets are convinced the European Central Bank (ECB) will cut rates once again when they meet on Thursday. Compared to the Federal Reserve, the ECB seems to have it under control when it comes to its monetary policy, with the June rate cut being key in setting the mood amongst European investors. For the past few months, it seems like markets have had full confidence in the ECB’s monetary path, whilst the Fed has endured questions about its reliability as a central bank. This confidence in the ECB has enabled European assets to maintain a positive bias even when market jitters saw global assets turn red.

Since the last rate cut in June, the ECB has said it remains data-dependent – and with the latest data seeming to suggest a cooling economy, it may be the perfect backdrop for another rate cut. President Lagarde said back then that she had decided to lower rates not because the economy was in dire need of a cut, but because she wanted to get the ball rolling and be more pre-emptive, allowing the central bank more wiggle room in the future. The market has responded well to this, as it means the ECB is more forward-looking, rather than being too focused on finding the perfect conditions to start cutting rates (which is what the Fed seems to have been doing).

Source: Refinitiv

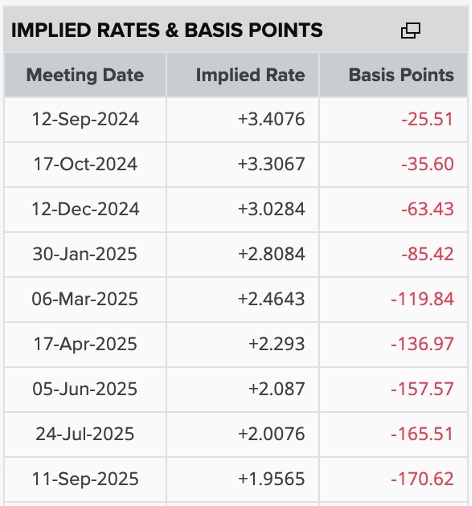

As shown above, markets expect the ECB to ease rates 63 basis points by the end of the year. This means that after this week’s expected cut, there could be one, maybe two more on the horizon. The Fed’s expectations are almost double that, with 110 basis points of cuts priced in over the next few months. This serves to show that markets remain more confident in the ECB than the Fed right now. Expectations of further easing in the US compared to Europe are contributing to the unwinding of the EUR/USD carry trade, which is likely to keep the pair supported. For the next 12 months, markets expect 170 bps of cuts from the ECB versus 238 from the Fed.

However, these expectations will depend on guidance from the central banks – and it is unlikely that we will get many updates from Lagarde this week. She will probably reiterate that “rates will remain sufficiently restrictive for as long as necessary”. The updated economic projections will be key, with focus on softer inflation if the easing period is to continue.

Meanwhile, growth continues to be sluggish in the Eurozone, with Germany still the main underperformer as compared to other countries like Spain and France. So even as rate cuts seem like a given, the pace of these cuts is still uncertain, which is likely to lead to speculation and drive market volatility over the coming months.

For the immediate future, the question is whether the ECB will decide to cut rates again in October. Historically, once a central bank starts cutting, the cycle is pretty quick. But as opposed to previous easing cycles, the base case this time is not a recession, which is causing central banks to drag out the rate cuts in order to get more up-to-date data before making decisions. However, with increased focus on excessive monetary policy restrictiveness, the ECB may be inclined to cut two months in a row, before assessing the situation further in December. That said, the data doesn’t seem to support this view right now, so unless Lagarde hints at a rate cut in October, it’s likely that markets will lean towards a December cut until further data can be assessed.

With regards to EUR/USD, the impact of a rate cut will likely be limited, as it is already priced in by markets. Instead, the focus will probably fall on the central bank’s communication. Any hints at an October rate cut may trigger some market jitters, as could an emphasis on stubborn services inflation.

However, it is probable that the US CPI report on Wednesday and FOMC meeting next week will have a greater impact on the short-term direction for EUR/USD. The lack of clarity from the August jobs report has left markets still unsure as to whether the central bank will cut 25 or 50 bps when it meets on Wednesday next week. The current pricing is leaning in favour of 25, but the CPI report could change that. If the market becomes more dovish, then we may see the dollar and yields pulling back, allowing EUR/USD to try and recover some of the lost ground over the past few days.

Past performance is not a reliable indicator of future results.

Disclaimer: This is for information and learning purposes only. The information provided does not constitute investment advice nor take into account the individual financial circumstances or objectives of any investor. Any information that may be provided relating to past performance is not a reliable indicator of future results or performance. Social media channels are not relevant for UK residents.

Spread bets and CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 84.01% of retail investor accounts lose money when trading spread bets and CFDs with this provider. You should consider whether you understand how spread bets and CFDs work and whether you can afford to take the high risk of losing your money.