Русский

Русский

- Nonfarm payrolls report and European flash CPI to shape rate cut bets

- ISM PMIs to also be important for Fed expectations and US dollar

- Canadian employment and Chinese PMIs also on the agenda

Fed hawks rear their ugly heads

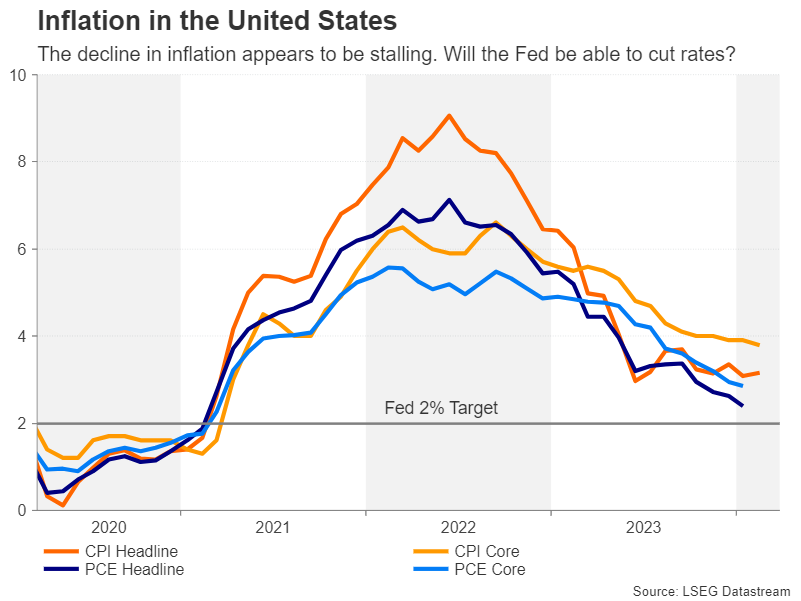

The March round of policy meetings reinforced June as the likely date when most central banks will begin cutting rates. Yet, doubts remain about whether or not inflation is on a sustainable path downwards, especially in the United States.

Although FOMC members maintained their projection of three rate reductions this year, they appear to have become more reluctant to commit to a specific timeframe for cutting rates. Inflation in the US has stalled around 3.0%, while the labour market remains very tight.

The worry is that cutting rates pre-emptively under such settings could refuel inflationary pressures. From the Fed’s perspective, the damage to its credibility would be greater in such a scenario than if it were to keep policy restrictive for longer than necessary.

But for the markets, the base case of a soft landing is imperative to feeding risk appetite so any change to that outlook risks putting an end to the rally on Wall Street and possibly giving the US dollar a leg up. The best hope for investors therefore is that the incoming data will be neither too hot, nor too cold.

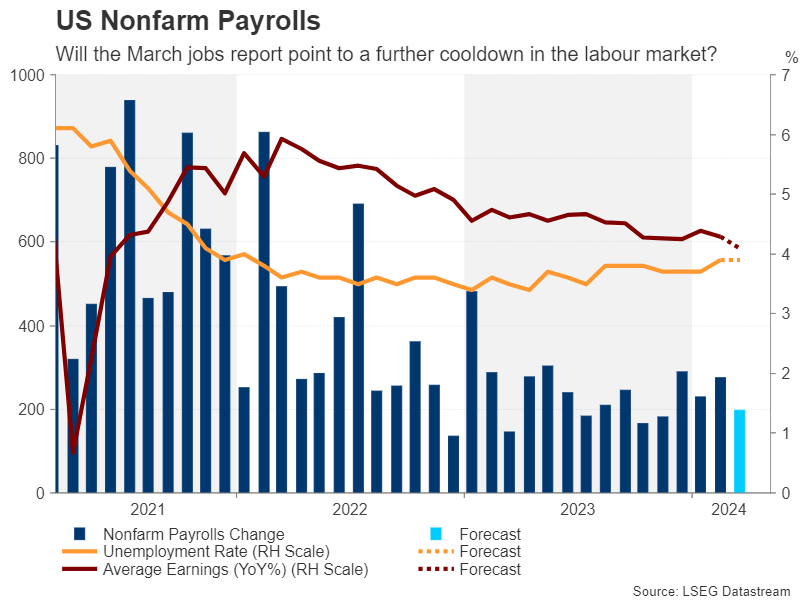

Is the US labour market really cooling?

That’s mostly been the case for the labour market, although it has been cooling down so gradually that it has kept the Fed on edge about overheating concerns. But the slowdown became more apparent in February when the unemployment rate ticked up to 3.9% and wage growth moderated to 4.3% y/y.

Jobs growth has stayed solid, however, with nonfarm payrolls increasing by 275k. The forecast for March is that the economy added 198k new jobs and the jobless rate held steady at 3.9%, while average hourly earnings growth is expected to have eased to 4.1% y/y.

Friday’s data will be preceded by the ISM PMIs. The manufacturing PMI is due on Monday and the services one on Wednesday. The former is anticipated to have improved slightly in March, but the latter is projected to have ticked lower.

If there’s a broadly positive set of figures, particularly if there’s a hotter-than-expected NFP print, this would likely deal a further blow to rate cut bets, providing another boost to the dollar.