Stocks edge higher on trade relief, but optimism wanes

Stocks edge higher on trade relief, but optimism wanes

The boost to global risk appetite following the US-China trade “ceasefire” seems to have been short-lived. Even though US stock markets closed higher, they did surrender a decent part of their gains late in the session, and futures tracking the likes of the S&P 500 are pointing to a notably lower open today. Moreover, Asian equities closed mostly in the red, while the defensive yen is outperforming on Tuesday, all signals that investors took the trade news with a pinch of salt. Perhaps market participants are coming to terms with how vague the accord really was, particularly considering the discrepancies between the US and Chinese statements; all that was agreed was to continue talking, which may not mean that much in the big picture.

Dollar extends pullback, looks to Fed speakers

The greenback remains on the back foot, trading lower against all its major peers today, even despite a robust ISM manufacturing PMI yesterday. The initial catalyst for the dollar’s weakness was the trade truce, which led investors to unwind some of their defensive bets. Interestingly though, the US currency didn’t manage to recover as the trade-related optimism started to fade, mainly because US bond yields also declined amid this reversal in sentiment, diminishing some of the dollar’s carry appeal.

Looking ahead, expectations around monetary policy may become a dominant force for the dollar again. Markets continue to price in just a single quarter-point Fed rate hike next year, which appears overly dovish considering the health of the US economy, even accounting for signs it may be slowing. Anything that alters this pessimistic narrative heading into the December 19 FOMC meeting could help the dollar to regain its footing.

New York Fed President John Williams speaks today, at 1500 GMT.

Oil rebound continues as hopes for an OPEC cut grow

Crude prices are extending their latest rebound, which was fueled by growing speculation OPEC and its allies are set to announce a fresh round of production cuts on Thursday. With investors looking increasingly certain the cartel will take action, the focus now turns to the magnitude of any cut. Market chatter suggests a reduction of the tune of 1-1.5 million barrels per day (bpd). Any signals pointing to a cut near the upper bound of this range may boost crude further, while anything below that range may bring them under renewed selling interest, given that expectations for a sizeable reduction are probably baked into prices already.

While it’s difficult to predict the exact magnitude of a cut, note that a very substantial one that causes prices to surge would most probably infuriate the US administration. Hence, Saudi Arabia – the de-facto OPEC leader – may ultimately opt to avoid that route, and instead deliver a more “middle-of-the-road” reduction simply to stabilize prices.

RBA a touch more upbeat, but no policy change in sight

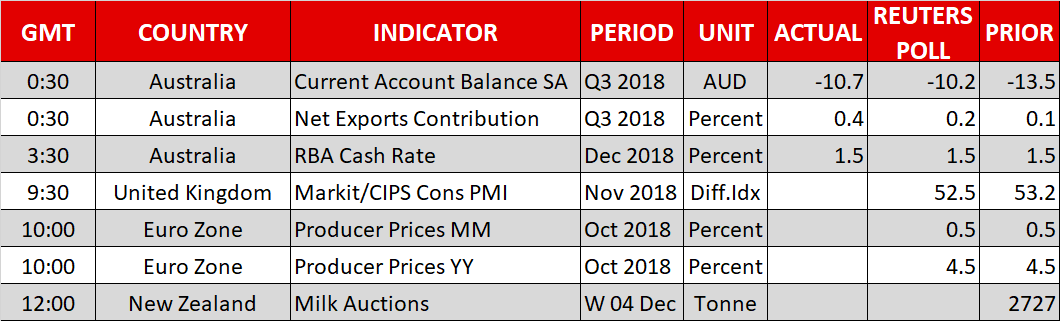

The Reserve Bank of Australia (RBA) kept its policy rate unchanged overnight. While there were no major changes to the accompanying statement, the overall tone was slightly optimistic. Policymakers highlighted continued progress in the labor market and wage growth, but also noted household consumption remains a source of uncertainty. As usual though, there was nothing to suggest a policy change is imminent. The aussie ticked higher on the news but given the RBA’s overall neutral bias, its direction going forward may hinge mainly on the evolution of risk sentiment, trade tensions, and commodity prices.

Other highlights for today

The key release today is the UK construction PMI for November, which is expected to have declined. That may weigh on the pound a little, though the overarching driver for the currency will probably remain the Brexit saga. In this respect, UK lawmakers will begin debating the Brexit deal today.

In New Zealand, the bi-weekly milk auction will be important for the kiwi, which touched a fresh 5-month high versus the dollar earlier today.

As for the speakers, BoE Governor Carney will testify before Parliament at 0915 GMT on the economic impact of Brexit.

Origin: XM