Here are the latest developments in global markets:

Here are the latest developments in global markets:

FOREX: The dollar is flat against a basket of six major currencies on Tuesday, holding on to the sizeable gains it recorded in the previous session, when it touched a fresh 17-month high. The yen was the second-best performer to start the week, behind the dollar, amid broad-based risk aversion in markets that fueled demand for defensive assets. Meanwhile, the euro underperformed even the pound, with euro/sterling increasingly becoming a function of which currency weakens faster, amid Italian and Brexit uncertainties.

STOCKS: US markets closed much lower, with the decline being led by the tech sector. The S&P 500 (-1.97%), Dow Jones (-2.32%), and Nasdaq Composite (-2.74%) felt the heat of a report suggesting Trump is set to escalate the trade conflict with China further, beyond the realm of tariffs. Apple (-5.04%) was caught in the eye of the storm, after three of its suppliers issued warnings about weakness in iPhone sales. Sentiment seems to have turned around though, as futures tracking the S&P, Dow, and Nasdaq 100 are all flashing green, pointing to a higher open today of around +0.6%. Asia was mixed on Tuesday, with Japan’s Nikkei 225 (-2.06%) falling, but the Hang Seng in Hong Kong staged a rebound (+0.46%). European indices were set for a higher open, according to futures.

COMMODITIES: Oil fell alongside equities, as the risk aversion in markets combined with an IEA report that oil demand will be severely impacted from electric cars by 2040 added to concerns around oversupply, pushing WTI and Brent to fresh multi-month lows. Speculation that OPEC may cut its production was not enough to alter sentiment, with President Trump in fact tweeting that he hopes Saudi Arabia and OPEC won’t reduce their production. In precious metals, dollar-denominated gold fell for a 7th straight session yesterday despite the risk-off environment, as the surge in the US dollar apparently outweighed haven demand. It is currently trading just above the $1,200 per ounce handle.

Risk aversion was the underlying theme during the late US session on Monday, with major US stock indices such as the S&P 500 falling by around 2.0%, and defensive assets such as the yen and the dollar attracting haven inflows. In terms of catalysts, a media report suggested the Trump administration may broaden its conflict with China beyond tariffs, and instead use export controls as well as indictments to counter intellectual property theft. Markets appear to have taken the news as a signal Trump is preparing to escalate the dispute, instead of laying the groundwork for a solution ahead of his G20 meeting with Xi Jinping at the end of the month.

Elsewhere, the British pound went for a rollercoaster ride. It dropped initially on reports PM May’s Cabinet is unhappy with her Brexit plans, then rebounded on a report that the “main elements” of an exit treaty text are ready, only to fall back down after a spokesman for the PM said the latter report should be treated with “skepticism”. The moves underscore that sterling is currently a hostage to incoming headlines, and suggest price action may stay choppy until there is some clarity, particularly on the Irish border issue.

Interestingly, the pound managed to gain against the battered euro, which fell across the board as investors cut their long exposure in anticipation of Italy submitting its revised budget proposal to the EU today. Italian politicians remain adamant about sticking to their deficit targets, thus setting the stage for a showdown with the Commission. Hence, political uncertainty looks set to remain elevated for a while, and the ultimate question may be how far the Commission is willing to take this standoff, as taking it too far via imposing fines for instance risks nurturing anti-EU sentiment even further.

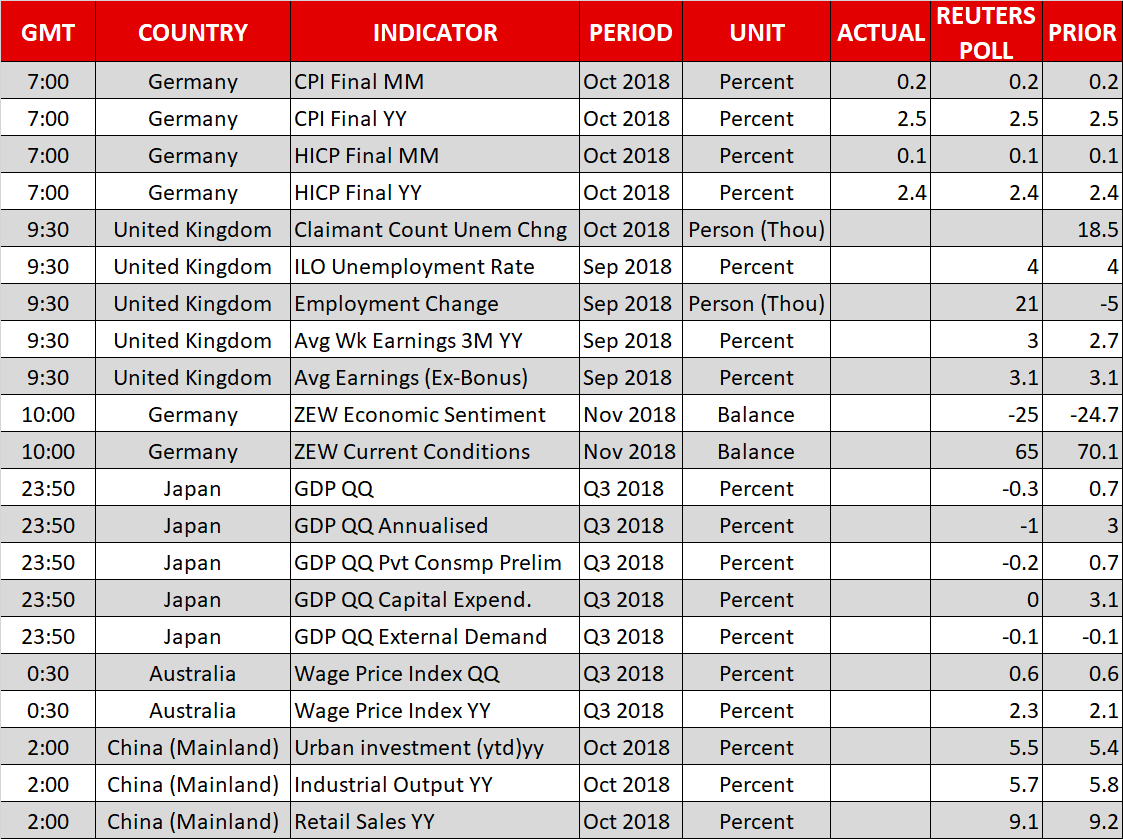

UK employment figures are the data highlight during Tuesday’s European session. Elsewhere, Brexit and Italian politics are ranking high in terms of importance, having the capacity to lead to sharp movements in FX markets.

At 0930 GMT, UK numbers on September employment, as well as October’s number of individuals claiming unemployment benefits, will be made public. The focus will again be on wage growth, which can stoke inflation expectations. In this respect, the three-month average of average weekly earnings is anticipated to pick up to 3.0% annually, notably above August’s 2.7% and at its highest since September 2015. Excluding bonuses, average earnings are projected to expand by 3.1%, the same as in August and matching their highest since January 2009.

Meanwhile, the economy is predicted to have added 21k positions, which compares to a reduction by 5k in August’s print, while the unemployment rate is forecast to remain at the multi-decade low of 4.0% for the fourth straight month.

Better-than-anticipated data are likely to help sterling advance, and vice versa, though again the dominant force underlying the pound’s movements is likely to be any Brexit headlines – there are mixed signals on this front, with sentiment for a deal oscillating from positive to negative. For the record, important data on inflation and retail sales out of the nation will follow on Wednesday and Thursday respectively.

Euro-related, the ZEW institute’s surveys gauging investor sentiment in Germany, the eurozone’s largest economy, will be hitting the markets at 1000 GMT. Both the economic sentiment and current conditions indices are expected to deteriorate in November compared to October. In particular, the former is anticipated at its worse since August 2012, at -25.0, and the latter at its lowest since late 2016, at 65.0. Trade uncertainty emanating from the Sino-US dispute and the prospect for a disorderly Brexit have been factors weighing on German investor morale in the past.

Greater potential to move the euro on Tuesday will be news having to do with Italy’s budget. The country faces a deadline set by the EU today to provide revised spending plans that align with EU rules. Italian officials do not seem willing to give in to demands and theoretically they could face fines. The “fine-route” is unlikely to be taken though; a “kick the can down the road” approach will likely materialize, keeping the euro hostage to updates moving forward.

Trade developments will also be monitored. The latest news suggest that China’s Vice Premier will visit the US to prepare the ground for a meeting between Presidents Trump and Xi later in November; the two are expected to meet at the G20 summit at the end of the month.

Fed policymakers Brainard (permanent FOMC voting member – 1500 GMT), Kashkari (non-voter in 2018 – 1500 GMT) and Harker (non-voter in 2018 – 1920 GMT) will be making public appearances today. Elsewhere, ECB Vice President de Guindos will be giving a speech at 1900 GMT.

It is of note that numerous key readings will be made public during Wednesday’s Asian session. Specifically, Japanese GDP figures (due on Tuesday at 2350 GMT) and Australian wage growth data (Wednesday – 0030 GMT), both for Q3. China will be on the receiving end of numbers on fixed asset investments, retail sales and industrial production, all for October (Wednesday – 0200 GMT).

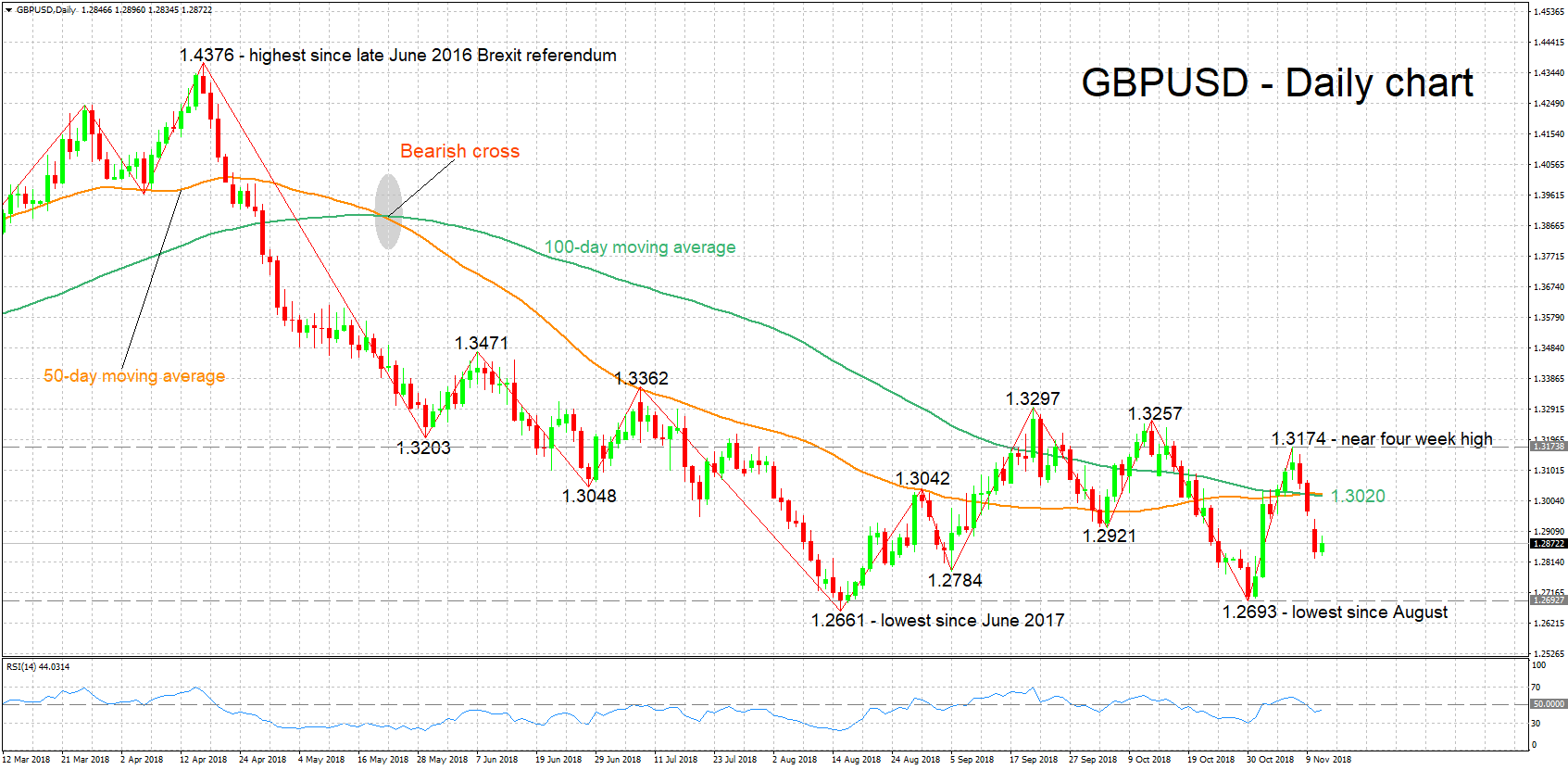

GBPUSD lost roughly 300 pips after touching a near four-week high of 1.3174 last week. The RSI retreated to enter bearish territory below 50, indicating a shift in momentum to the downside.

Upbeat employment figures out of the UK or positive Brexit news are expected to boost the pair. Resistance to gains may take place around a previous bottom at 1.2921, before the attention turns to the zone around 1.3020, this being the current level of the 100-day moving average line – the area around this captures the 1.30 round figure, a previous top (1.3042) and bottom (1.3048), as well as the 50-day MA which has roughly converged with the 100-day one. Higher still, last week’s peak of 1.3174 would increasingly come within scope.

On the downside and in case of disappointing data or Brexit complications, support could emerge around a previous bottom at 1.2784. Further below, 1.2693, the lowest since mid-August would be eyed, with the more than one-year nadir of 1.2661 lying not far below.

Origin: XM