Here are the latest developments in global markets:

Here are the latest developments in global markets:

FOREX: The US dollar index is slightly higher on Thursday (+0.08%), recouping some of the losses it posted in the previous session as safe-haven bets on the currency were scaled back following news the US and China are set to hold new trade talks. The risk-sensitive aussie surged, while the loonie also advanced after Mexico’s economy minister played up the prospect of a US-Canada trade deal. Elsewhere, the euro and sterling were little changed, ahead of the BoE and ECB policy meetings today.

STOCKS: Wall Street had a mixed session on Wednesday, with optimism for a fresh round of US-China trade talks being counterbalanced by a broader retreat in the tech sector. The Dow Jones (+0.11%) and the S&P 500 (+0.04%) managed to post some marginal gains, though the tech-heavy Nasdaq Composite (-0.26%) fell, being weighed by giants like Facebook (-2.37%) and Apple (-1.24%). Asia traded on a more cheerful note on Thursday, with nearly every major index being in the green. In Japan, the Nikkei 225 (+0.96%) and the Topix (+1.11%) recovered some of their recent losses, as did the Hang Seng in Hong Kong (+2.05%). In Europe, futures tracking all the major indices are pointing to a relatively flat open today, with the only exception being the Italian FTSE MIB, which is expected to open lower.

COMMODITIES: Oil prices pulled back on Thursday, giving back the gains recorded in the previous session after the weekly EIA inventory data showed a larger-than-expected drawdown in US crude stockpiles. WTI is lower by 0.68% at $69.81 per barrel today, while Brent lost 0.44% to trade at $79.38/barrel. In precious metals, gold is fractionally lower (-0.03%) at $1204 an ounce. The dollar-denominated metal rose yesterday, as a retreat in the US currency rendered it more appealing for investors using foreign currencies. That said, price action remains within a narrow sideways range between $1,214 and $1,189, and a break in either direction is needed to determine the short-term bias.

The US dollar retreated against all its major peers on Wednesday as market participants unwound some of their safe-haven exposure to the greenback, following reports that the US government has proposed another round of trade negotiations with China. In an environment where investors were anticipating a fresh round of tariffs between the two to be announced at any moment, this news likely helped to ease some concerns around further escalation, and possibly brought the prospect of a negotiated solution back on the radar.

Major US stock indices jumped on the news, but pulled back in the following hours amid a rout in tech stocks. Meanwhile, the Aussie – which has been acting as the barometer for trade tensions given Australia’s dependence on exports – surged, distancing itself from the 2 ½ year lows it touched last week against the dollar. The currency also got a lift from robust Australian employment data released earlier overnight. Meanwhile, the safe-haven Japanese yen spiked lower on the trade-talk news as risk appetite improved, but still managed to hold onto some of its prior gains to end Wednesday’s session higher overall against most of its major counterparts.

In NAFTA-land, the Canadian dollar was back in the spotlight, posting gains across the board amid renewed optimism that a fresh trilateral trade accord may be agreed soon. The move came after the Mexican economy minister Guajardo said he sees a “high chance” of a US-Canada deal, boosting speculation for such an outcome and hence reducing the NAFTA risk-premium on the loonie. The negotiations will continue today in Washington, and as usual, the loonie will remain ultra-sensitive to any fresh headlines.

Elsewhere, movements in the FX market were relatively muted, with investors appearing somewhat reluctant to initiate major new positions on the euro or sterling before they receive updated guidance from both the Bank of England and the European Central Bank later today (see below). In emerging markets, the Turkish lira could attract interest today, as the nation’s central bank is expected to deliver a sizeable rate increase to help stabilize the battered currency and rein in double-digit inflation.

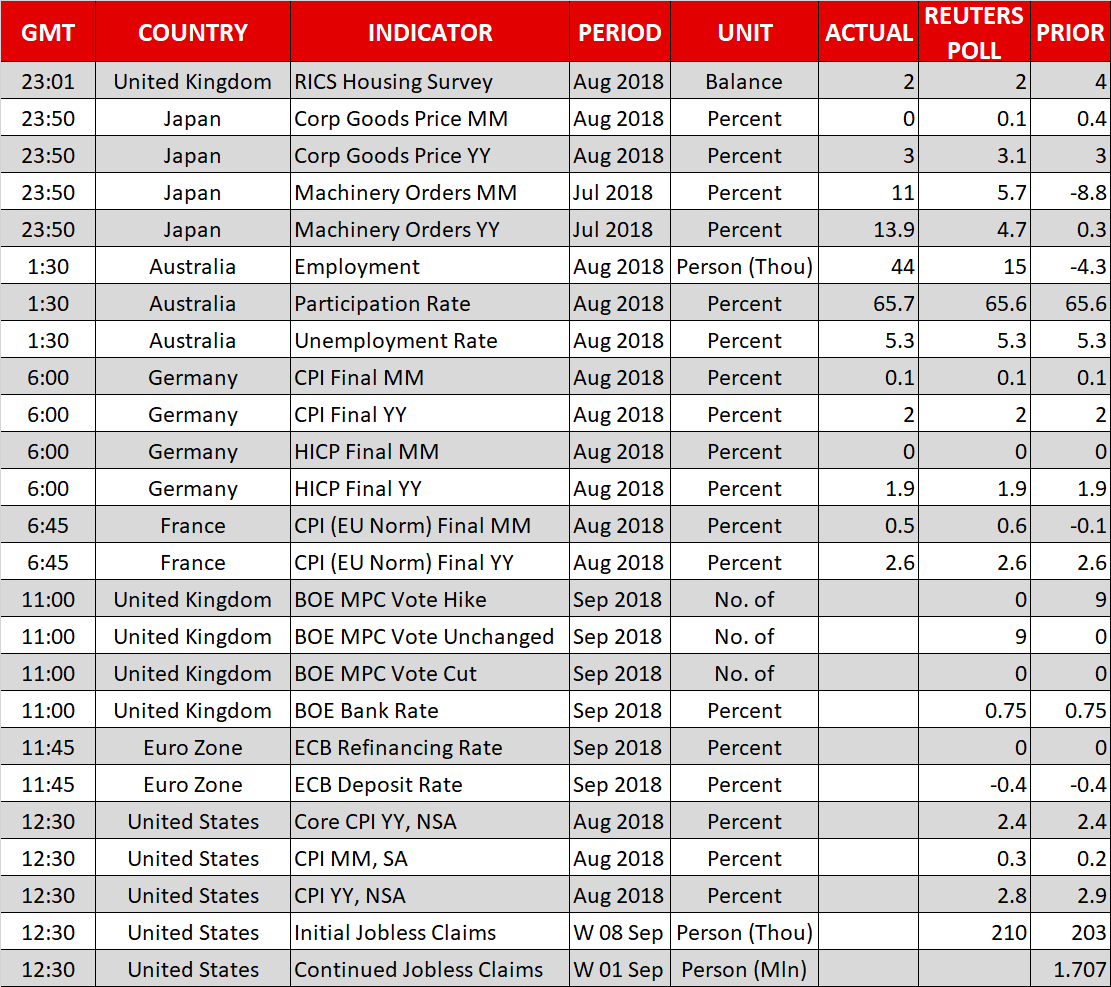

The European Central Bank and the Bank of England will be concluding their meetings on monetary policy on Thursday. Beyond policy decisions, US inflation data as gauged by the consumer price index (CPI) will be released, while deliberations revolving around trade will also be monitored.

On the trade front, news that the US is seeking a fresh round of talks with China are boosting sentiment. Meanwhile, discussions for a new NAFTA deal between the US and Canada are set to continue today.

Both the Bank of England and the European Central Bank are expected to keep their policies unchanged when they complete their meetings today at 1100 GMT and 1145 GMT respectively. The focus will thus turn on their guidance. Will the former maintain its view for “gradual and limited” rate increases, or will it deviate from that position? Brexit commentary by the Bank will also be closely watched, as well as any developments for a UK-EU deal of course.

Turning to the ECB, new economic projections will be eyed, with sources indicating the Bank will lower its economic growth forecasts even as it plans to scale down on stimulus, ending its asset purchases by year-end. A press conference by ECB President Draghi will follow at 1230 GMT; the ECB chief does not tend to shy away from market-sensitive comments.

Elsewhere, in EM-space which is seen as posing threats to developed markets lately, Turkey’s central bank will also be making a policy decision today at 1100 GMT. The Bank is expected to hike rates, though there’s uncertainty as regards the magnitude of the move. The more hawkish the central bank, the greater appreciation is to be anticipated in the lira, with the opposite holding true as well; it should also be taken into account though, that a sharp rise in rates is likely to weigh on economic activity later on.

Out of the US, headline CPI due at 1230 GMT is forecast to come in at 0.3% m/m in August, from July’s 0.2%. This would put the annual pace of growth at 2.8%, slightly below the 2.9% experienced in the two previous months, this being a high last seen in early 2012. Core CPI that excludes volatile items is projected to remain constant at 2.4% y/y. A data beat could be seen as more conclusively putting on the table two more rate increases by the Fed in 2018, hence supporting the dollar, and vice versa. It is of note that yesterday’s data on August factory inflation as measured by the producer price index (PPI) negatively surprised. Lastly, weekly jobless claims data out of the world’s largest economy are due at the same time.

Atlanta Fed President Raphael Bostic (voting FOMC member in 2018) will be talking on the economic outlook and monetary policy at 1700 GMT.

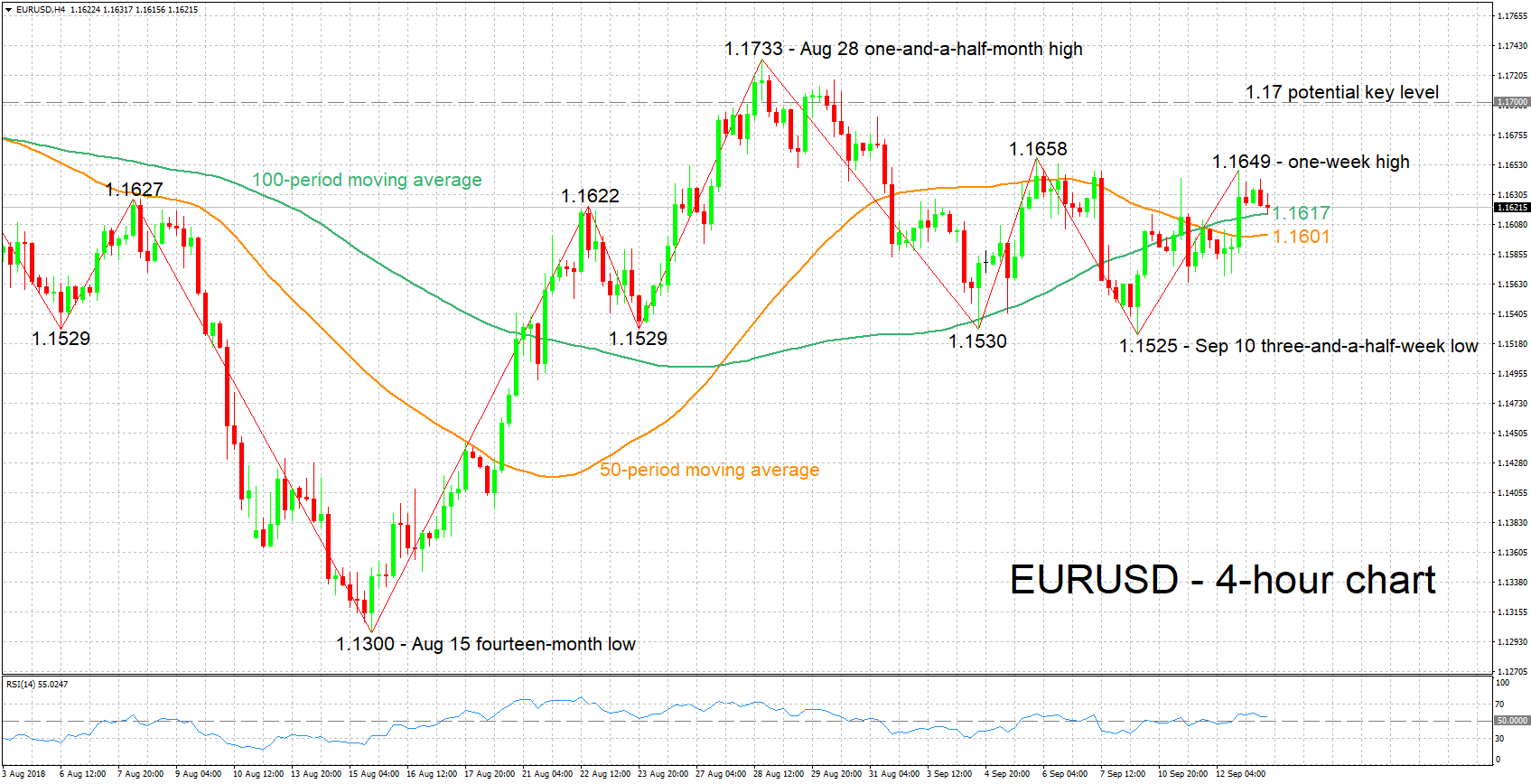

EURUSD is trading around 30 pips below Wednesday’s one-week high of 1.1649. The RSI is largely moving sideways, projecting a mostly neutral picture in the short-term.

An upbeat ECB relative to market expectations will likely lift the pair. Resistance to gains may come around yesterday’s one-week high of 1.1649, with the area around it encapsulating another peak from the recent past at 1.1658. Further above the 1.17 round figure would be eyed, with the late August one-and-a-half-month high of 1.1733 lying not far above.

Conversely, a relatively downbeat ECB is expected to lead to a falling EURUSD. Immediate support to losses seems to be taking place around the current levels of the 100- and 50-period moving average lines at 1.1617 and 1.1601 correspondingly. Steeper losses would turn the attention to the zone around the three-and-a-half-week low of 1.1525 from September 10.

CPI data out of the US can also move the pair.

Origin: XM