Here are the latest developments in global markets:

Here are the latest developments in global markets:

FOREX: The US dollar is little changed against a basket of six major currencies on Wednesday, holding onto the gains it recorded in the previous session. Staying in North America, the Canadian dollar was a major underperformer yesterday, touching a one-and-a-half-month low against the greenback ahead of the Bank of Canada’s policy decision later today (1400 GMT). EM currencies also came under broad selling pressure, weighed on by news that South Africa had entered a technical recession, with the rand losing roughly 3.0% against the dollar on Tuesday.

STOCKS: US markets edged lower on Tuesday on their first session back from a holiday, as weakness in industry leaders like Facebook (-2.60%) and Nike (-3.16%) added to concerns over an imminent escalation in the Sino-American trade standoff. Fresh worries around emerging markets may have played a role too. The tech-heavy Nasdaq Composite (-0.26%) led the decline, with the S&P 500 (-0.17%) and the Dow Jones (-0.05%) posting more moderate losses. Sentiment seems to have remained sour, as futures tracking the Dow, S&P, and Nasdaq 100 are pointing to a notably lower open today. Asia was a sea of red on Wednesday as well. In Japan, the Nikkei 225 and the Topix declined by 0.51% and 0.77% respectively, while in Hong Kong, the Hang Seng plunged by a whopping 2.33%. In Europe, all the major indices were set to open lower today, futures suggest.

COMMODITIES: Oil prices came crushing down on Tuesday, and are also in the red today, after the anticipated supply disruptions in the Gulf of Mexico did not materialize. WTI is down by nearly 1.0% on Wednesday while Brent is lower by 0.73%, as US oil platforms did not sustain much damage from tropical storm Gordon, suggesting that any production outages will likely be limited. In precious metals, gold is up by 0.1% today, hovering close to the $1,192/ounce mark. The dollar-denominated yellow metal posted considerable losses yesterday as the US currency climbed.

Dollar bulls were once again an unstoppable force yesterday, with the greenback advancing across the board as a renewed selloff in emerging markets (EM), jitters around trade tensions, and stellar US data enhanced the allure of the US currency. The crisis in EM deepened after GDP data unexpectedly showed South Africa slipped into a technical recession in Q2, triggering another rotation out of EM assets and into dollar-denominated ones. A surprisingly strong US ISM manufacturing PMI for August – which touched its highest level in 14 years – aided the positive sentiment, with the looming imposition of fresh US tariffs on China as early as tomorrow likely fueling haven demand for the dollar as well.

Meanwhile in Canada, the loonie drastically underperformed, touching fresh one-and-a-half-month lows against the dollar ahead of the BoC’s rate decision later today (see below). Interestingly enough, implied rate-hike odds for the BoC’s upcoming meetings remained largely stable in recent days, which suggests the loonie’s weakness is owed primarily to concerns around trade and specifically, the risk of failing to reach a NAFTA deal. In this respect, the US-Canada negotiations resume today.

On the Brexit front, EU chief negotiator Michel Barnier reportedly shot down PM Theresa May’s Chequers plan, labelling it as “not acceptable”. Instead, the EU has proposed a Canada-style free trade agreement, though the details of such a plan are not clear yet. All in all, it appears PM May’s hard-fought plan over which two ministers resigned is now dead in the water, amplifying the likelihood the talks may remain stuck in limbo for longer. Indeed, market-implied odds suggest the next BoE rate increase will only come in November 2019 – a pricing so pessimistic relative to the healthy state of the UK economy it probably incorporates expectations Brexit issues will keep policymakers away from touching the hike button.

Overnight, aussie/dollar briefly spiked higher following stronger-than-expected Australian GDP data for Q2. However, the pair quickly gave back its gains to trade even lower as the greenback advanced, remaining stuck near one-and-a-half year lows.

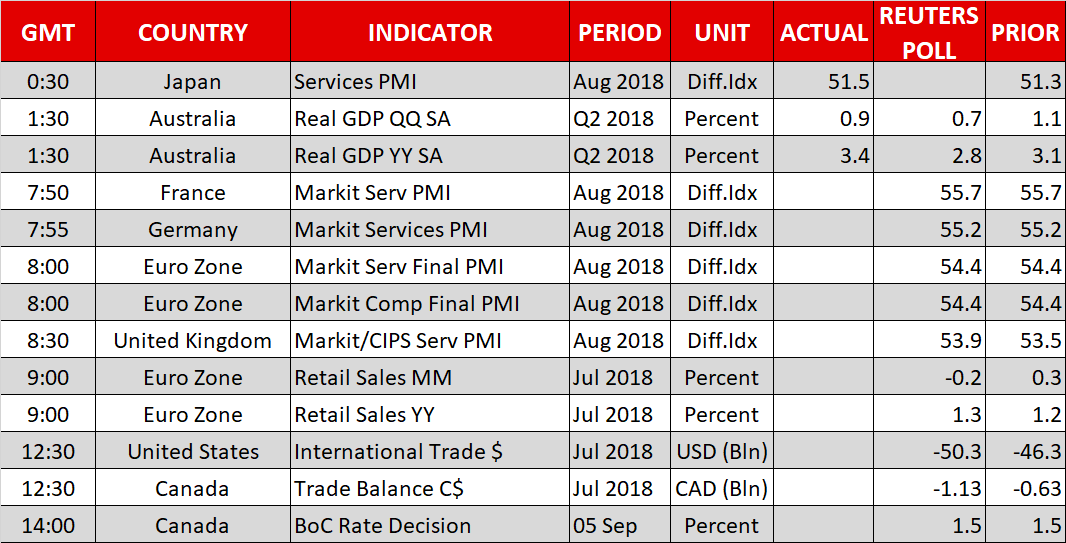

A Bank of Canada rate decision, US trade data, the UK services PMI and eurozone retail sales are on the agenda on Wednesday. In the meantime, trade tensions and emerging market angst persist.

The PMI reading for the all-important for the UK economy services sector will be made public at 0830 GMT. The measure, which comes after disappointing PMI prints on manufacturing and construction earlier in the week that weighed on sterling, is anticipated to rise to 53.9 in August from 53.5 in July.

Earlier in the day, at 0800 GMT, the eurozone will also be on the receiving end of PMI data for the services sector, as well as the composite PMI that blends manufacturing and services. These, though, would pertain to the final prints and are unlikely to cause significant positioning in euro pairs, given that the preliminary readings tend to be reliable; both the services and composite PMIs are projected to stand at 54.4, unchanged from their flash estimates. Germany and France, the eurozone’s two largest economies, will see their respective PMI figures hitting the markets at 0755 GMT and 0750 GMT correspondingly.

Also out of the eurozone, retail sales for July are due at 0900 GMT. Month-on-month, sales are expected to contract by 0.2% after rising by 0.3% in June. This would put the year-on-year pace of growth at 1.3%, above June’s 1.2%.

The Bank of Canada’s rate decision is due at 1400 GMT. The central bank is anticipated to hold rates steady and pave the way for a rate increase during next month’s meeting; Canadian OIS see a 76% chance for a 25bps rise in rates during the October gathering. A shock-hike today will be met with a surging loonie, while on the other side of the spectrum, a dovish-hold of rates at current levels (i.e. no signaling for a hike next month) will likely lead to a tumble in the Canadian currency. No press conference by Governor Stephen Poloz will follow after the completion of the meeting.

Trade developments – whether Canada will come to an agreement with the US on a new North American trade deal – are also of importance for the loonie’s direction. Meanwhile, Canadian trade data for July are due at 1230 GMT, the same time the US will see the release of its own trade numbers for July. The US trade deficit is projected to widen to $50.3 billion, from $46.3bn in June.

Remaining on trade, the Sino-US spat still lingers one day before the public comment period on additional tariffs on $200 billion of Chinese imports ends; President Trump signaled last week that his administration will proceed with new tariffs as soon as this period ends.

In EM, the Argentine peso, South African rand and the Turkish lira are some of the currencies that are coming under pressure. The situation will be monitored for potential spillover effects as well.

In terms of policymakers’ appearances: ECB member Peter Praet will be making a speech at 0830 GMT. Meanwhile, remarks by FOMC members James Bullard (non-voting FOMC member in 2018 – 1320 GMT), John Williams (permanent voter – 1430 GMT) and Neel Kashkari (non-voter – 2000 GMT) are on the agenda as well.

In equities, executives from Facebook and Twitter, as well as Google’s top lawyer will be testifying before Congress on Wednesday on Russia meddling in the 2016 US presidential election.

In energy markets, weekly API data on US crude stocks are due at 2030 GMT.

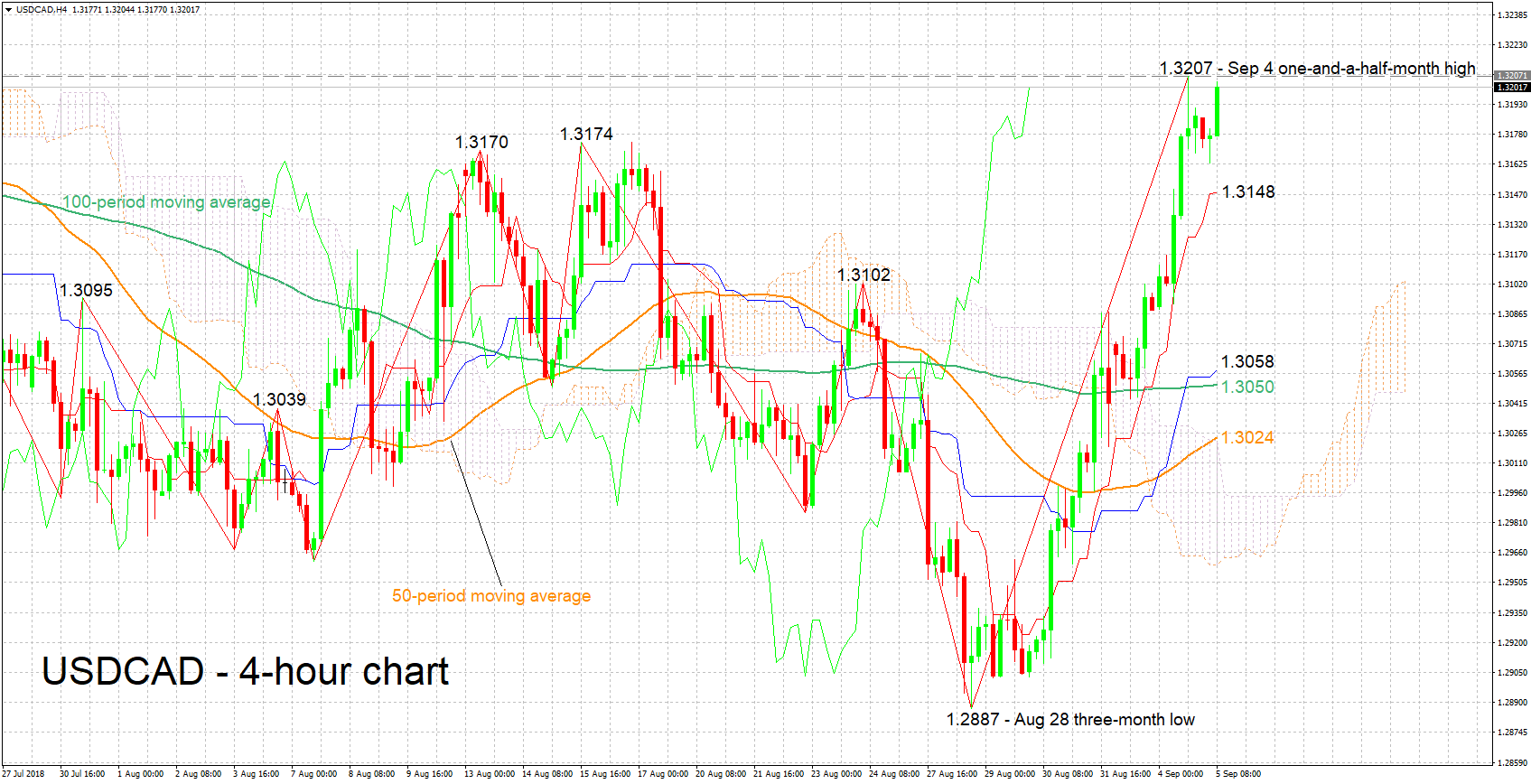

USDCAD is currently eyeing Tuesday’s one-and-a-half-month high of 1.3207. The Tenkan- and Kijun-sen lines are positively aligned in support of a bullish short-term picture.

A hawkish Bank of Canada relative to market expectations later today will likely boost the loonie, pushing USDCAD lower. Support to declines may come around the current level of the Tenkan-sen at 1.3148; the zone around this also includes a couple of peaks from the recent past. Further below, support could occur around the 1.31 round figure which also encapsulates a few tops from previous weeks, while further down the area around the Kijun-sen at 1.3058 would be eyed.

On the upside and given a relatively dovish Canadian central bank, immediate resistance seems to be taking place around yesterday’s high of 1.3207. Steeper gains would increasingly bring into scope the 1.33 handle.

Trade developments can also move the pair.

Origin: XM