Here are the latest developments in global markets:

Here are the latest developments in global markets:

FOREX: The US dollar index is lower by a little over 0.2% on Thursday, pulling back after touching a new 13-month high in the previous session, aided by risk aversion and encouraging US retail sales prints. The Japanese yen is also on the retreat, after news that the US and China will hold another round of trade talks in late August curbed demand for haven assets.

STOCKS: Wall Street closed in the red on Wednesday, as a selloff in tech shares dragged the broader market lower. The tech-heavy Nasdaq Composite led the selloff (-1.21%), after disappointing earnings results from Chinese tech behemoth Tencent Holdings shook the tech sector. The S&P 500 and Dow Jones closed down by 0.76% and 0.54% respectively. Sentiment appears to have reversed overnight though, following reports the US and China will seek trade negotiations. The Dow, S&P, and Nasdaq 100 are all set for a higher open today, according to futures. Asia was a sea of red on Thursday. Japan’s Nikkei 225 (-0.05%) and Topix (-0.64%) ended lower, as did the Hang Seng in Hong Kong (-0.98%). In Europe, futures tracking all the major indices are pointing to a notably higher open today, though not for the Italian FTSE MIB.

COMMODITIES: Oil prices plunged on Wednesday, weighed on by a stronger US dollar, a risk-averse mood in markets, and a surprisingly large buildup in the weekly EIA crude inventory data, instead of the anticipated drawdown. WTI and Brent are a little higher on Thursday, by 0.11% and 0.38% respectively, likely aided by news that the US and China will hold another round of trade talks in late August. In precious metals, gold is marginally higher by 0.1% today. That said, the yellow metal touched a new 17-month low of $1,160 per troy ounce earlier in the Asian trading session before rebounding, confirming that the broader downtrend is back in force.

The US dollar and the Japanese yen recorded another round of gains on Wednesday as investors’ risk appetite turned sour once more. Risk aversion took hold after Chinese tech giant Tencent reported disappointing earnings results, with an escalating political standoff between Washington and Ankara likely adding to concerns after Turkey doubled its tariffs on iconic US goods yesterday, including American cars and tobacco. Hence, investors sought the safety of the Japanese yen, with the greenback also attracting some haven inflows under the view that the US economy is probably better prepared than most of its peers to weather any storm that may arise. The dollar index briefly touched a fresh 13-month high.

Sentiment seems to have reversed on Thursday, though, with risk appetite being boosted by overnight reports that the US and China will make another attempt at resolving their trade dispute through negotiations, scheduled for late August. The news sent the yen and greenback lower during the Asian trading session. The euro – which in recent months had been hurt by signs of escalation in the trade dispute – capitalized on the news, staging a recovery against its major peers today. Similarly, risk-sensitive currencies like the aussie and kiwi got a lift today, though both continue to hover not far above their respective multi-year lows.

The fact that the two sides are still actively pursuing a negotiated solution is an encouraging sign by itself, and suggests the endgame is probably still some kind of “grand accord”, not a prolonged trade war. That said, judging from the relatively moderate market reaction, investors likely took the news with a pinch of salt, recalling that similar talks earlier in the summer did not ultimately bear fruit. Instead, they may have even increased distrust, as the Chinese side perceived the US to be backtracking from issues they believed they had agreed on. For now, the prospect of a deal still appears somewhat remote, considering the large rifts between the two sides.

Elsewhere, the British pound posted new one-year lows against both the dollar and the yen yesterday, while it also retreated against the euro. With the EU-UK negotiations resuming today, Brexit is likely to move firmly back into the spotlight.

Turning to EM, the Turkish lira regained some ground in recent sessions, with dollar/lira falling back below the 5.80 handle, helped by reports that Qatar will invest as much as $15 billion in the country. The latest rebound is also being attributed to profit taking on prior short positions, as well as the central bank tightening liquidity through its daily operations.

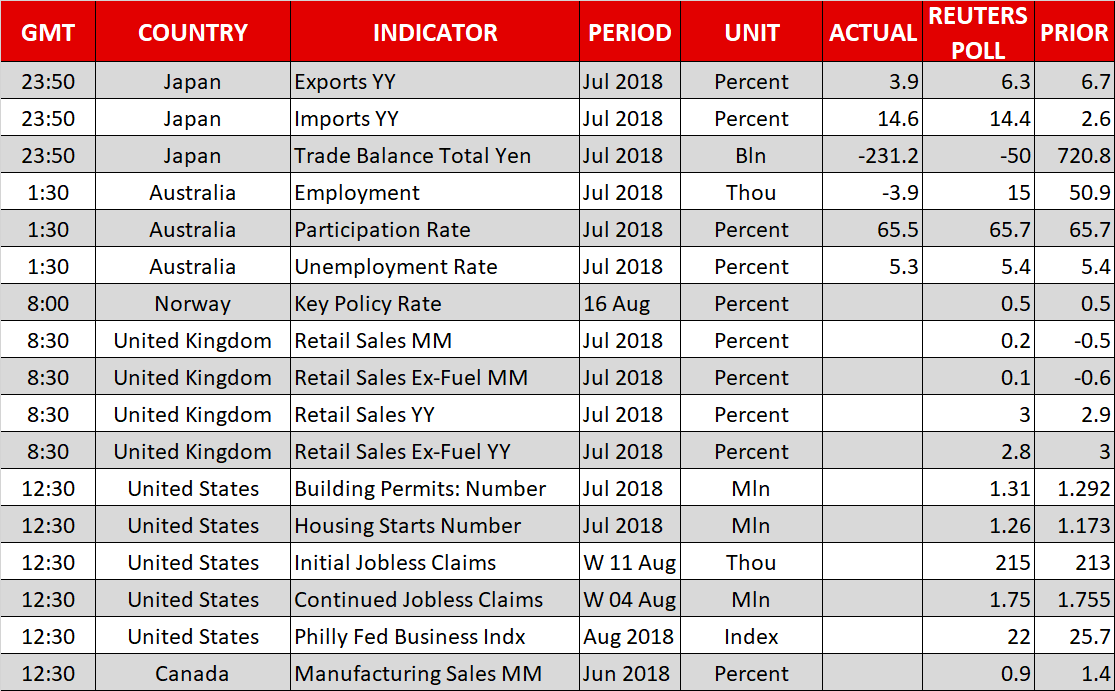

Retail sales figures out of the UK, as well as US housing data will be on tap on Thursday. In the meantime, trade developments will be in focus after news that China and the US will be holding trade talks in late August, while any Turkey-related news will also be attracting attention. In addition, Brexit talks will be resuming.

The Norwegian central bank’s interest rate decision will be made public at 0800 GMT. A “hawkish hold” of rates is perhaps the meeting’s most likely outcome, with the central bank maintaining its benchmark rate at 0.50% and reiterating that it remains on track to hike rates at next month’s meeting. Also in the Nordic sphere, the Swedish Finance Minister Magdalena Andersson will today be presenting the country’s new economic forecasts and spending plans for the coming years as Sweden heads for general elections on September 9.

UK retail sales for July are due at 0830 GMT. Sales are projected to grow by 0.2% m/m, returning into positive territory after declining by 0.5% in June. This would put the annual pace of expansion at 3.0% from June’s 2.9%. Core retail sales that exclude fuel are also anticipated to record positive monthly growth after contracting in June. Sterling pairs though may prove more sensitive to any Brexit updates with another round of talks between the UK and the EU getting underway today in Brussels.

Out of the US, housing starts are expected to have grown by 7.4% in July, after declining by 12.3% in June to touch a nine-month low. Meanwhile, July’s building permits, weekly jobless claims data, as well as August’s Philly Fed Business index will be released at the same time; the Philly Fed survey, which in the past recorded a notable deterioration on the back of rising worries over the US-China trade spat, is projected to reflect a worsening compared to July’s print.

Canadian manufacturing sales for June are due at 1230 GMT.

China’s Ministry of Commerce saying that it had received an invitation from the US for talks to be held between the two parties in late August is a positive development for risk sentiment. Should this story receive traction, with the world’s two largest economies shying away from protectionist actions, then it is likely for riskier assets and perceived risk-on currencies such as the aussie to appreciate. The situation in Turkey will also be monitored though, as it can also affect sentiment in the markets.

In equities, Walmart and Nvidia will be releasing quarterly results on Thursday; the former before the US market open and the latter after the closing bell.

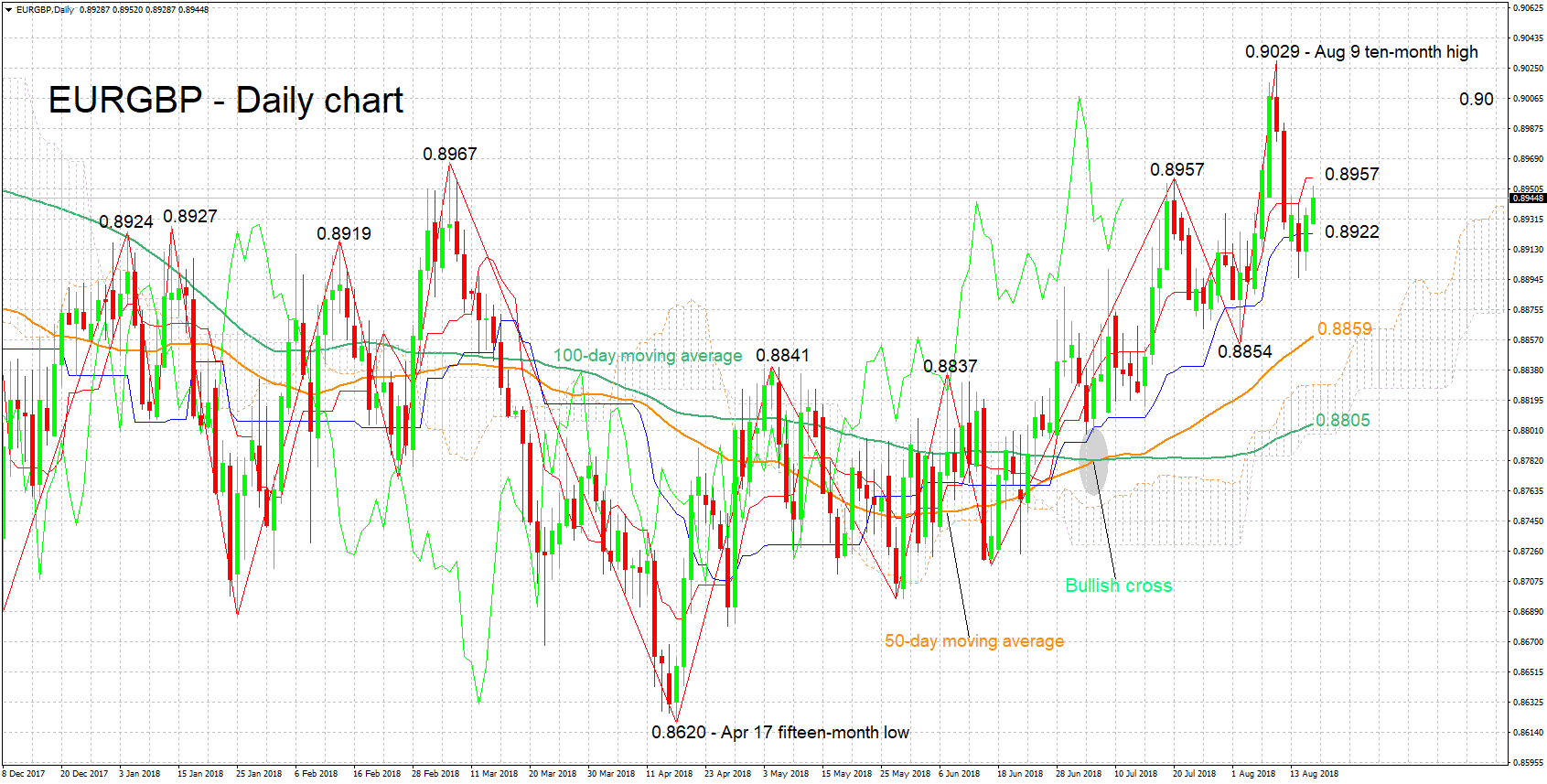

EURGBP is trading roughly 90 pips below last week’s 10-month high of 0.9029. The Tenkan-sen remains above the Kijun-sen in support of a bullish bias, though the flat Kijun-sen is signaling an easing positive momentum.

Upbeat UK retail sales figures or an indication from Brussels that the UK and the EU are getting closer to a deal on Brexit, are expected to push the pair lower. Immediate support may take place around the Kijun-sen at 0.8922 – including the 0.89 handle – with steeper losses increasingly bringing into scope the area around the current level of the 50-day moving average line at 0.8859.

Conversely, weaker-than-anticipated retail sales numbers or higher odds for a no-deal Brexit are likely to lead to a firmer EURGBP. Initial resistance to advances may occur around the Tenkan-sen at 0.8957. Further above and given a break above the 0.90 round figure, the 10-month high of 0.9029 from August 29 would come in focus.

Origin: XM