Here are the latest developments in global markets:

Here are the latest developments in global markets:

FOREX: The US dollar index is marginally higher on Thursday, attempting to extend the massive gains it posted in the previous session. Dollar/yen is up by 0.21%, having touched a fresh high for the year earlier. Meanwhile, the loonie dropped on Wednesday as oil prices collapsed, erasing the gains it posted after the BoC raised rates, to trade much lower in the aftermath.

STOCKS: US markets closed lower yesterday, as trade concerns remained the dominant theme. Some spectacular losses in oil prices also pushed energy stocks lower. The Dow Jones dropped by 0.88%, the S&P 500 by 0.71%, and the tech-heavy Nasdaq Composite by 0.55%. However, sentiment seems to have turned around, as futures tracking the Dow, S&P, and Nasdaq 100 are all currently signaling a higher open today. The shift in appetite was evident in Asia too, which was a sea of green. Japan’s Nikkei 225 and Topix climbed by 1.17% and 0.46% respectively, while in Hong Kong, the Hang Seng gained 1.48%. Europe was a similar story, with futures pointing to a higher open for all the major benchmarks today.

COMMODITIES: Oil prices collapsed on Wednesday, with WTI falling by 5.0% and Brent collapsing by 6.9% in the day. In dollar terms, WTI dropped by $3.73, and Brent by $5.46. The massive losses followed news that Libyan oil exports will soon return to normal levels, bringing back a significant chunk of supply to the market. A surge in the US dollar, data showing Saudi Arabia continues to raise its production, and concerns around the impact of trade tensions on oil demand, may have played a role too. In precious metals, gold plunged yesterday as well, pressured by a strengthening US dollar. Since the yellow metal is denominated in dollars, a strengthening greenback renders it less attractive for investors using foreign currencies. It’s currently trading near $1,244, not far above its lows for the year, at $1,238.

The Bank of Canada (BoC) raised interest rates yesterday, as was widely anticipated. The tone of the accompanying statement was neutral overall, acknowledging that the Canadian economy is strong and will likely require higher interest rates over time, but also that uncertainty surrounding trade tensions has risen lately. The loonie jumped on the decision. It appears investors were expecting a much more worried tone by policymakers, and hence even a neutral stance may have come as somewhat of a hawkish surprise.

That didn’t last though. The loonie gave back all its gains even before Governor Poloz’s press conference started, and continued to trade much lower in the subsequent hours. The losses appear to have been driven more by movements in the oil market and a surge in the US dollar, rather than anything Poloz said. Even though the weekly EIA crude inventory data showed a massive drawdown, that was dwarfed by news that recent supply disruptions in Libya have been resolved, and the nation will soon ramp up its crude exports. WTI plunged by almost $4, posting its largest one-day drop in two years. Since Canada is a major oil exporting economy, the collapse in oil was seen as undermining the nation’s export revenue, hence pushing the loonie lower.

Meanwhile, the US dollar gained across the board yesterday, with some relatively hawkish comments from Chicago Fed President Evans potentially aiding the move. He appeared quite relaxed about further hikes, saying that whether the Fed raises rates once or twice more this year is not that important in the big picture. Coming from someone who is usually ultra-cautious, his remarks likely amplified expectations for two more hikes this year. Stronger-than-expected US PPI data may have played a role too. Dollar/yen is 0.21% higher on Thursday, posting a new high for the year of 112.37.

The euro reached a seven-week high against the yen, which has been losing ground despite escalating trade tensions, after a media report suggested the ECB could raise rates earlier than September 2019. It said some policymakers believe their forward guidance does not rule out a hike as early as July 2019. The ECB minutes today will be scrutinized for any color on the subject.

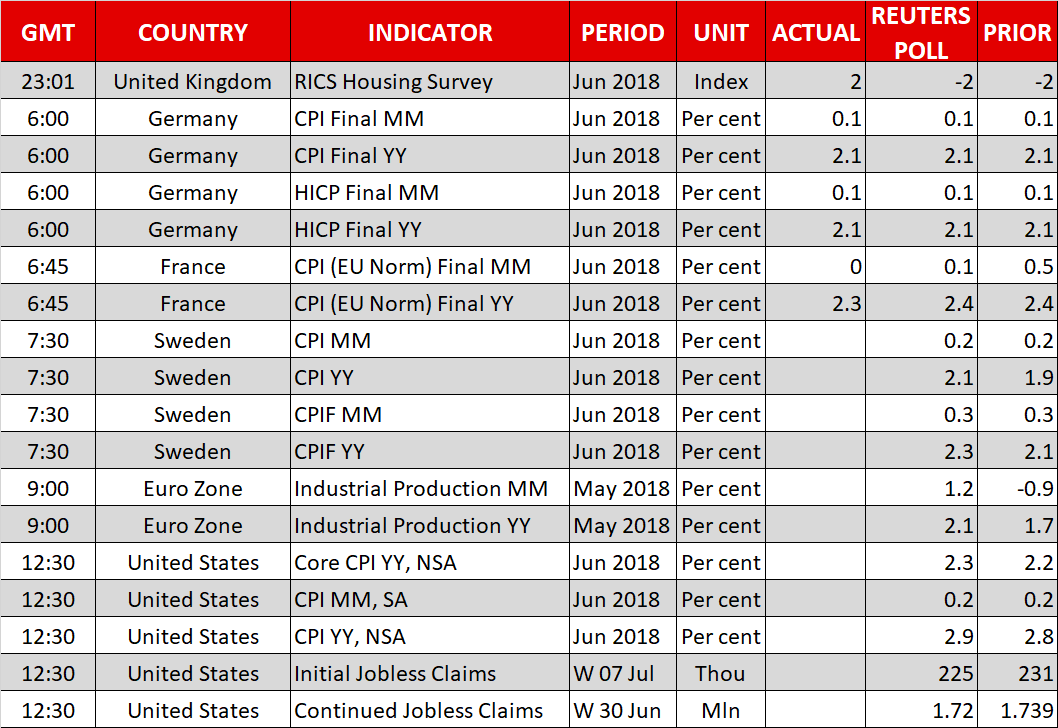

The releases that are likely to prove the most market sensitive out of Thursday’s calendar are the ECB’s official record of its latest meeting, as well as US consumer price data. The release of a White Paper on Brexit by the UK government could also gather attention.

Krona pairs will be gathering attention as Swedish inflation will be hitting the markets at 0730 GMT, while at the same time the Swedish central bank will be publishing the account of its latest monetary policy meeting.

At 0900 GMT, eurozone industrial production data for May will be made public. Output is anticipated to accelerate on both a monthly and yearly basis compared to April. Perhaps of more importance for euro pairs though, will be the ECB’s minutes pertaining to its June meeting due at 1130 GMT. During that meeting, the central bank surprised by committing to end its asset purchases by year-end. However, it left an overall “dovish taste” to the markets by pushing back expectations regarding the timing of the delivery of a rate hike, leading to a sell-off in the euro. As the record of the meeting is made public, investors will want to assess the strength of the commitment to end asset purchases, as well as maybe when a rate increase is most likely to materialize.

Concerns over global trade were also likely discussed during the ECB’s June meeting, and any comments on the issue and the risks posed by increased protectionism will be generating interest. Meanwhile, any updates on the US-China spat during Thursday’s trading will be closely monitored.

The US will be on the receiving end of June inflation data as gauged by the consumer price index (CPI) at 1230 GMT. Month-on-month, headline CPI, is projected to grow at 0.2%, the same as in May, while year-on-year growth is expected to reach a six-and-a-half-year high of 2.9% (from 2.8% in May). Core CPI, which strips out volatile food and energy items (the rise in oil prices is supportive of a higher headline CPI reading), is forecast to grow at 2.3%, from 2.2% in May. Yesterday’s producer price index (PPI) beat supported the case for two more rate increases by the Federal Reserve as the year unfolds. Another positive surprise in today’s data is likely to further boost such expectations, consequently pushing the greenback higher. Lastly, weekly jobless claims data are also due out of the US at 1230 GMT.

In the UK, all eyes will be on the release of the much-anticipated Brexit White Paper by Theresa May’s government. While a 3-page outline of the agreement was already released on Friday, today markets will get a glance at the full 100-page document. The details will be studied to determine how “workable” and “realistic” the UK’s proposals are, with the verdict likely to have a sizeable impact on sterling. Should it be seen as a practical plan that increases the likelihood for a “smoother Brexit”, the pound could benefit, and vice-versa.

Philadelphia Fed President Patrick Harker, a non-voting FOMC member on 2018, will be speaking at 1415 GMT. In the meantime, a meeting between US Secretary of State Mike Pompeo and EU Foreign Policy chief Federica Mogherini at 1100 GMT might be of interest, especially in light of the recent developments relating to global trade.

In equities, Delta Air Lines will be releasing its quarterly results before today’s opening bell on Wall Street.

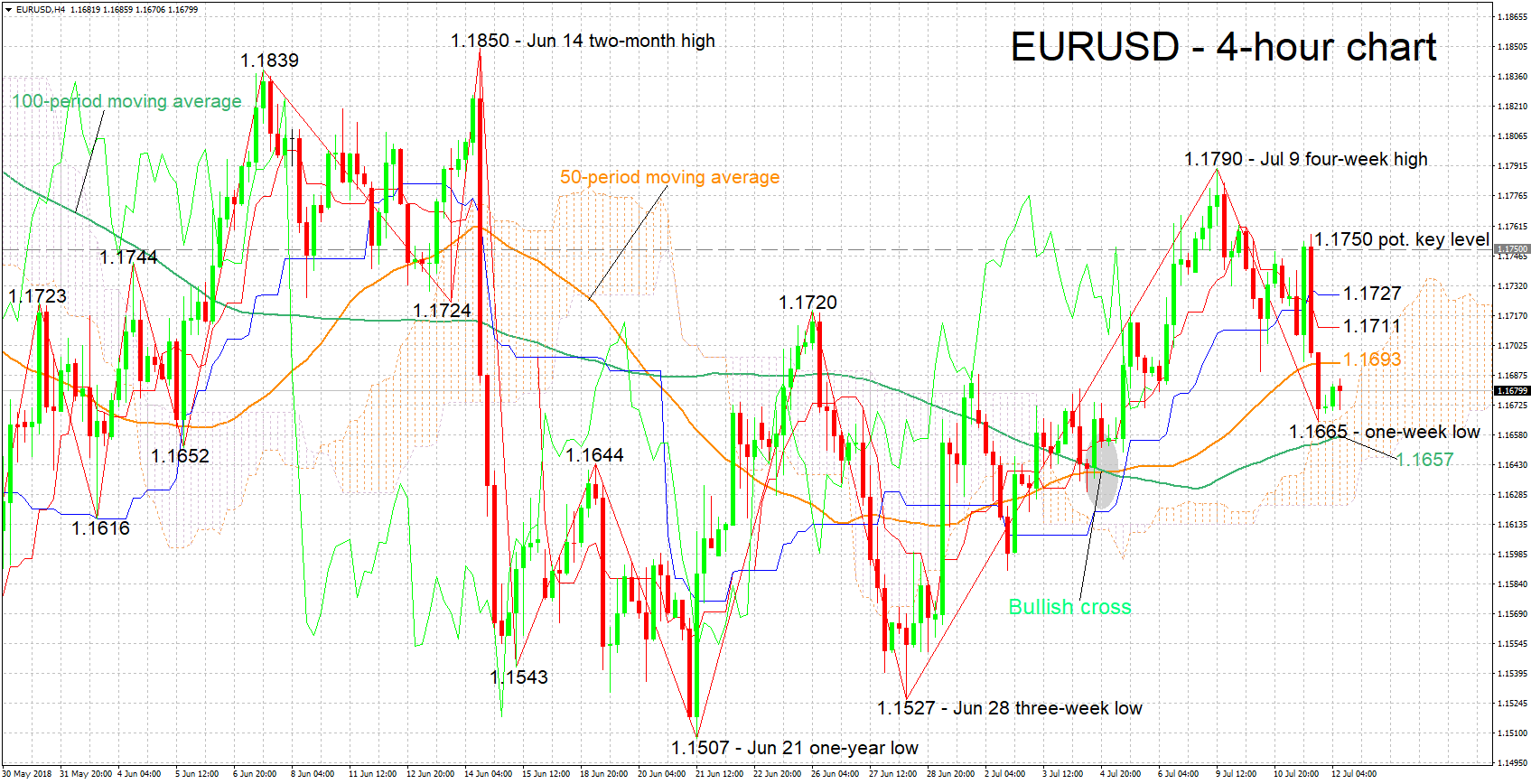

EURUSD has retreated from Monday’s four-week high of 1.1790, eventually falling to a one-week low of 1.1665 on Wednesday, while it is currently trading not far above the aforementioned trough. The Tenkan-sen is below the Kijun-sen, this being a signal for a bearish bias, though the two lines have flatlined, an indication that bearish momentum has lost steam. Overall, the near-term picture is looking bearish-to-neutral.

A more hawkish ECB than initially thought after the completion of June’s meeting, is likely to push the pair higher. Initial resistance to advances may come around the current level of the 50-period moving average line at 1.1693, including the 1.17 round figure. The current levels of the Tenkan-sen (1.1711) and Kijun-sen (1.1727) lie not far above and may act as resistance as well.

On the other hand, a relatively dovish ECB, is expected to exert selling pressure on EURUSD. A first-line of support to declines may occur from the area around the 100-period MA at 1.1657, which also encapsulates yesterday’s one-week low (1.1665), as well as the Ichimoku cloud top (also at 1.1665). The Ichimoku cloud bottom at 1.1623 would be eyed in case of steeper losses.

Eurozone industrial production and US CPI figures also have the capacity to move the pair.

Origin: XM