Here are the latest developments in global markets:

Here are the latest developments in global markets:

FOREX: The US dollar index – which measures the greenback’s performance against a basket of six major currencies – is down by 0.23% on Monday, following a slightly disappointing US employment report on Friday. Elsewhere, pound/dollar is up by the same amount, after the UK Brexit Secretary David Davis resigned his post.

STOCKS: Wall Street indices closed higher on Friday, after the US employment report for June showed that wage growth remains subdued. The tech-heavy Nasdaq Composite led the charge, climbing by 1.34%, while the S&P 500 and Dow Jones followed in its tracks, gaining 0.85% and 0.41% respectively. Moreover, futures tracking the Dow, S&P, and Nasdaq 100, are all pointing to a notably higher open today. Asia was a sea of green on Monday as well, with Japan’s Nikkei 225 and Topix up by 1.21% and 1.20% correspondingly. In Hong Kong, the Hang Seng jumped 1.71%. Europe was a similar story; all the major benchmarks are expected to open significantly higher, futures suggest.

COMMODITIES: Oil prices are up on Monday, with WTI and Brent crude advancing by 0.51% and 0.67% respectively. The oil market remains caught between multiple narratives, with expectations that major producers like Saudi Arabia will soon raise their production being counterbalanced by supply outages in Canada, Libya, and Venezuela. Moreover, tensions between the US and Iran are very high. Iran threatened to block a strategic oil-shipping waterway last week, and the US navy replied it will ensure freedom of navigation and flow of commerce. In precious metals, gold is up by 0.55% on Monday, currently trading near $1,259 per ounce, drawing strength from the continued correction lower in the US dollar.

The British pound opened with a small positive gap on Monday, following news that the UK Brexit Secretary, David Davis, has resigned. Davis criticized PM May’s new Brexit plan – which was agreed by the UK cabinet on Friday – indicating it would leave Parliament with a weak negotiating position. While many details are still unknown as the UK plan will only be made public later this week, it appears that it solves the thorny issue of the Irish border by establishing free trade for goods. Judging by the market reaction, investors likely interpreted the development as increasing the odds for a “softer Brexit”, as one of the leading Brexiteers left the administration and the negotiations may soon be able to move forward – if the EU accepts the plan, of course.

The dollar tumbled on Friday, following the US employment report for June, which was a touch softer than expected. While nonfarm payrolls came in above expectations, wage growth disappointed. Average hourly earnings rose at the same pace as previously in yearly terms, missing the forecast for a slight acceleration. The unemployment rate unexpectedly jumped to 4.0% from 3.8%, though that was probably owed to a similar jump in the labor force participation rate. Fed rate-hike odds barely moved; one more 25bps rate hike is fully priced in for this year, while markets see a 40% probability for a second one, according to the Fed funds futures.

On the trade front, while the US-China trade standoff escalated on Friday, with the two nations imposing tariffs on $34bn worth of products, markets paid little attention. US stock indices closed higher, while the Japanese yen – widely considered a haven asset – ended the day lower against the euro and the pound. The move was well-signaled in advance and hence, came as no surprise. What matters now, is whether the two sides will continue imposing measures on each other in tit-for-tat fashion, entering a vicious loop of escalation as neither wants to back down, or whether the prospect of more dialogue and negotiations will reappear.

In the commodity currencies, the loonie jumped on Friday after stronger-than-expected employment data from Canada sealed the deal for a rate increase by the BoC later this week. Meanwhile, aussie/dollar and kiwi/dollar are up by 0.48% and 0.22% respectively today, recovering some of the notable losses they posted recently.

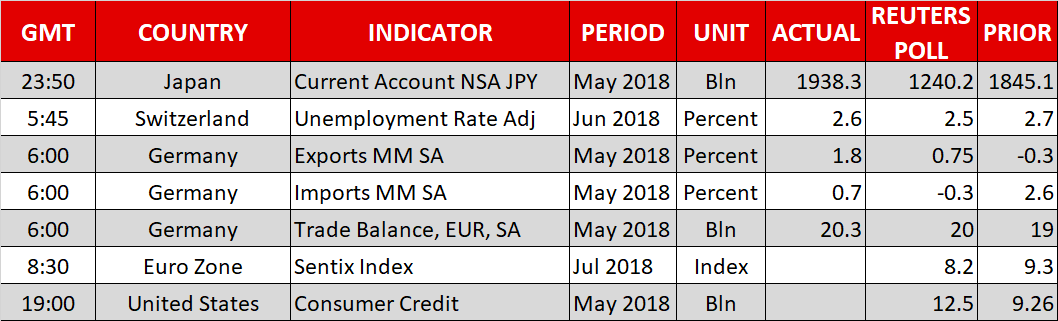

Monday’s calendar is a rather light one in terms of releases, featuring the Sentix index out of the eurozone and consumer credit data out of the US.

July’s Sentix index that gauges investor sentiment in the eurozone is slated for release at 0830 GMT. The measure is anticipated to record its sixth straight monthly decline. Specifically, it is projected to stand at 8.2, its lowest since September 2016. Political uncertainty in Italy and rising protectionist rhetoric on the front of global trade by the US have been factors weighing on investor morale in previous months.

US consumer credit data for May are due at 1900 GMT; a rise in credit is expected during the month.

Remaining in the background during Monday’s trading are concerns over global trade and Brexit-related uncertainty after the resignation of Brexit Secretary David Davis (see Major movers section).

ECB President Mario Draghi will be speaking at the EU Parliament’s ECON committee at 1300 GMT, while he will be returning to the rostrum at 1500 GMT.

Meanwhile, a news conference at 1300 GMT featuring German Chancellor Angela Merkel and Chinese PM Li Keqiang after German-Sino consultations might be of interest, especially in the aftermath of the latest trade developments.

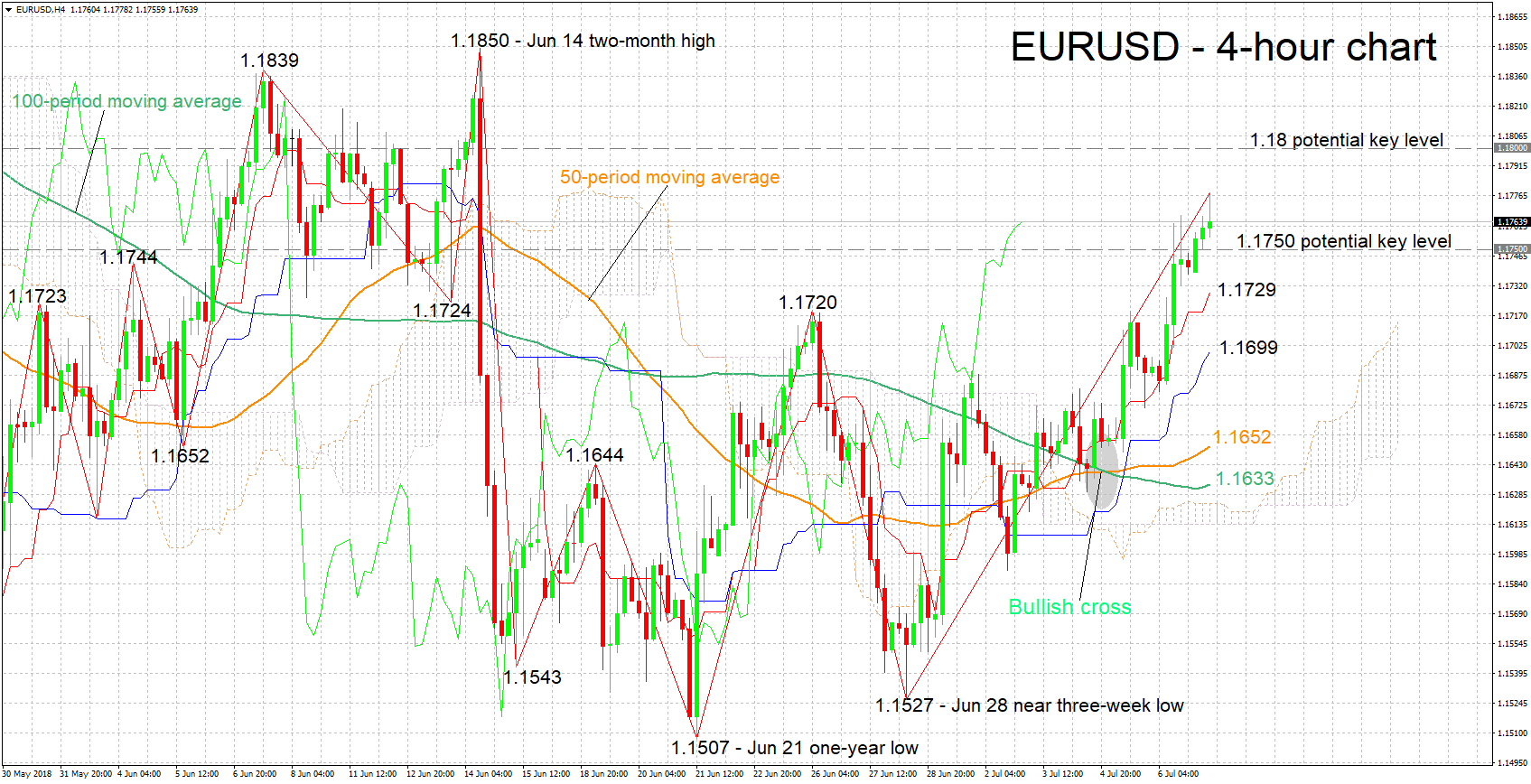

EURUSD has gained roughly 250 pips after touching a near three-week low of 1.1527 in late June. Earlier on Monday, it recorded a near four-week high of 1.1778. The Tenkan-sen remains above the Kijun-sen in support of a bullish short-term picture. The Chikou Span, though, may be pointing to an overbought market, the implication being that a near-term reversal is not to be ruled out.

The Sentix index does not typically act as a major market mover but still an upbeat report could boost the pair. Resistance to advances could come around the 1.18 round figure, before the attention starts to increasingly turn to the two-month high of 1.1850 from around mid-June.

On the downside and in case of a downbeat survey by Sentix, support could come from the zone around the 1.1750 level which was somewhat congested in the past. Notice this region failed to provide resistance earlier in the day and may instead act as support. Further below, the attention would turn to the areas around the current levels of the Tenkan-sen (1.1729) and Kijun-sen (1.1699) lines for additional support.

Origin: XM