Here are the latest developments in global markets:

Here are the latest developments in global markets:

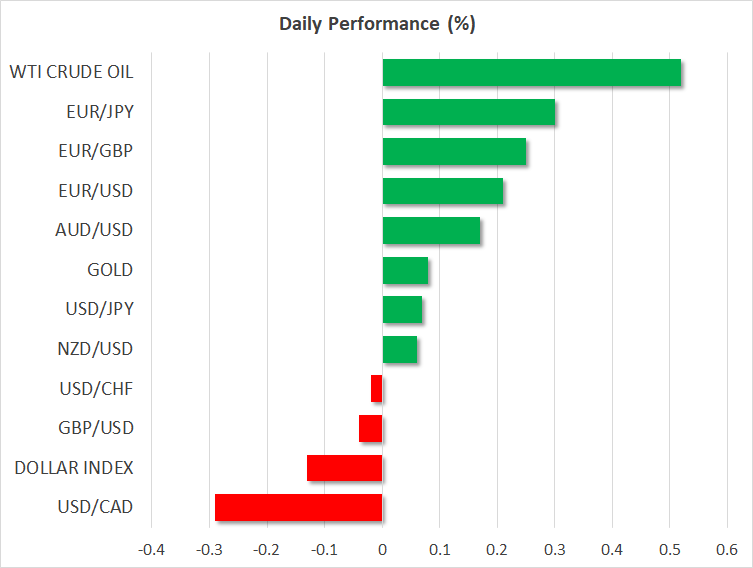

- FOREX: The dollar retained its strength against the yen, trading near a 1-½ -week high, finding support from rising US Treasury yields, while the euro was last flat on a weekly basis versus the greenback after advancing in the three preceding weeks. Pound/dollar stretched its uptrend to a fresh two-month high amid hopes that the EU and the UK were preparing the ground to take Brexit talks to the next level, entering trade discussions.

- STOCKS: The Nikkei 225 finished 0.4% higher, retreating from an earlier advance that saw it rise by 1.2% to reach its highest since 1992; Euro Stoxx 50 futures were 0.1% lower at 0744 GMT; Dow futures were flat, while S&P 500 and Nasdaq 100 equivalents both traded lower by 0.2%.

- COMMODITIES: Oil prices edged up after Friday’s OPEC/non-OPEC meeting confirmed the long-awaited extension of supply cuts through 2018. WTI crude rose by 0.51% to $57.69 per barrel and Brent jumped by 0.67% to $63.05. Gold was flat around three-week low levels at $1,275.22 per ounce.

Major movers: Dollar flat as Senate tax vote stalls; pound moves above $1.35

The dollar index was last steady at 92.93. On Thursday, Senate Republicans decided to postpone the tax bill vote for Friday after some members expressed worries about the sustainability of the tax bill version as is. With the cloud around the promised tax cuts getting darker, dollar/yen paused yesterday’s uptrend at 112.55 as a strong rally in the 10-year US treasury yields offset the dollar’s losses. Euro/dollar increased by 0.17% to 1.1922, while pound/dollar hit a fresh two-month high of 1.3548 following news that the EU and the UK were close to agreeing on two key elements involving the Irish border and the UK’s financial settlement to the block – the EU demands such key issues to be solved before Brexit negotiations move to trade talks after the EU summit in the mid-December.

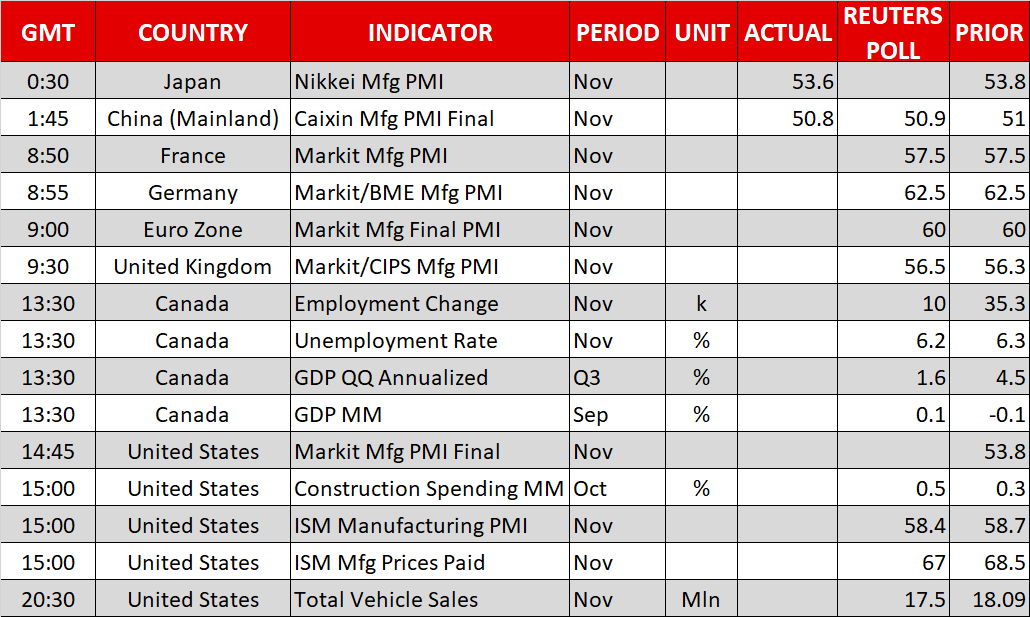

Day ahead: US tax bill vote, Canadian GDP & employment data and manufacturing PMIs from major economies to dominate attention

The eurozone will see the release of the November manufacturing PMI at 0900 GMT. However, given that the release pertains to the final estimate of the measure, it is not an eagerly awaited one. Manufacturing PMI is expected to remain unrevised relative to the flash reading and at its highest in almost seven years (at 60.0).

At 0930 GMT, the November Markit/CIPS manufacturing PMI out of the UK will be released. It is expected to stand at 56.5, its highest since August (September’s reading stood at 56.3). A reading above 50 signifies expansion in the sector.

Canada will see the release of important data pertaining to November employment (and unemployment) and growth in economic activity (Q3 and September’s) at 1330 GMT. GDP growth is expected to have slowed markedly in the third quarter to 1.6% on an annualized basis from the second quarter’s 4.5%. Today’s data have the capacity to steer market expectations as regards the timing of the delivery of the next rate hike by the Bank of Canada and consequently can lead to sharp movements in the dollar/loonie pair (among other loonie pairs).

In terms of US data, November’s final Markit manufacturing PMI will be released at 1445 GMT, with data on construction spending and ISM’s manufacturing PMI following at 1500 GMT. Undoubtedly though, most attention will be on the US Senate and the tax bill vote after yesterday deciding not to vote on the bill, continuing discussions today.

Among Fed speakers that could make some market-sensitive comments, St. Louis Fed President James Bullard will be giving a presentation on the US economy and monetary policy at 1405 GMT and Dallas Fed President Robert Kaplan (an FOMC voting member) will be participating in a Q&A session at 1430 GMT. Philadelphia Fed President Patrick Harker (also an FOMC voting member) will be talking about inclusive economic growth at 1515 GMT.

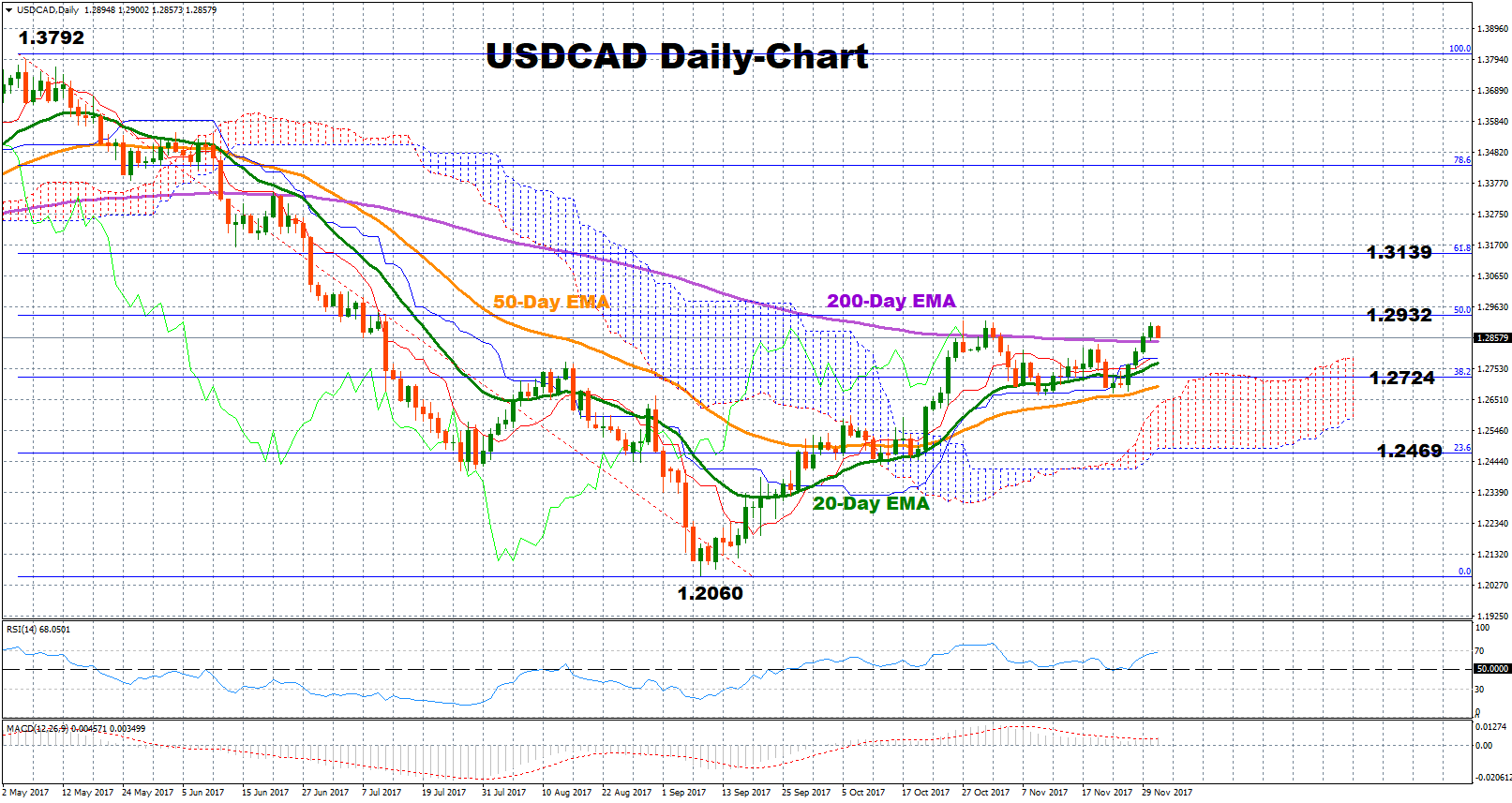

Technical Analysis: USDCAD sending bullish signals in the short-term

USDCAD has been moving sideways around a four-month high since the end of October but the pair maintains a bullish picture both in the short- and the medium-term as it still trends above the exponential moving average lines and the Ichimoku cloud. The RSI is also positively sloped and above 50, giving another positive signal for the short-term. Potential resistance levels could be found between the 50% and the 61.8% Fibonacci retracement levels of the downleg from 1.3792 to 1.2060 (1.2922-1.3125). Yet, USDCAD could postpone the bullish rally for a while if the Canadian data appear better than expected, crawling down to meet the 200-day EMA at 1.2845. Additional support levels could be provided by the 20-day EMA at 1.2777 and the 38.2% Fibonacci mark at 1.2724, before the 23.6% Fibonacci level of 1.2469 comes into view.

Origin: XM